Choose an Insurance Quote

Most Ontario households have spent over $15k on insurance in the past four years

KEY FINDINGS

- Ontarians spent $14K–$21K on insurance from 2022–2025. Toronto households spent $20,946 over four years.

- Insurance now takes 4% of median after-tax income. Toronto’s burden is highest at 5%, while Ottawa’s is lowest at 3%.

- Premiums surged across Ontario cities. Oshawa (+37%), London (+35%), and Ottawa (+35%) saw the steepest increases.

- 75% of insured households reported premium hikes. Many adjusted coverage or shopped around to manage costs.

- Bundling, telematics, and discounts can save up to 30% on premiums. These strategies help households offset rising premiums.

Insurance has shifted from a background bill to a core cost‑of‑living pressure.

Auto and home premiums have risen amid a perfect storm of higher claim severity, climate‑driven weather losses, crisis-level auto theft, rebuild‑cost inflation, more expensive vehicles and more.

According to data from the Rates.ca auto and home insurance quoter, households across Ontario spent between $14,000 and $21,000 on combined auto and home insurance over the past four years, depending on their city of residence.

Overall, insurance costs grew faster than wages and outpaced headline inflation through late 2025.

And Canadians are feeling it. In a national Leger survey commissioned by Rates.ca, 75% of insured households* reported premium increases over the last two years. Many have made adjustments to try to lower their bill, from shopping around to cutting coverage.

This report tracks what Ontarians paid for insurance from 2022 to 2025, and how households are responding to rising auto‑driven costs.

Toronto residents spent almost $21,000 on insurance over the past four years

Across six major Ontario cities, home and auto premiums rose every year from 2022 to 2025, but not at the same pace.

Toronto households faced the highest costs – their combined insurance costs rose from $4,850 in 2022 to $5,693 in 2025. As a result, each household’s annual premiums represented about 5% of the city’s median after‑tax income of $122,735.

For context, in 2023, the average household spent $8,659 on groceries, meaning the 2025 insurance bill is more than half of a year’s grocery spending.

Over four years they paid a total of $20,946.

Ottawa remains the most affordable city for insurance costs, with households paying $14,401 over four years — equal to 3% of the capital city’s median household after-tax income in 2025.

Here is how much households paid each year in insurance — and over four years:

Swipe horizontally to view full table →

| City | 2022 | 2023 | 2024 | 2025 | Total | Income burden in 2025 | 2022 to 2025 % increase |

|---|---|---|---|---|---|---|---|

| Toronto | $4,850 | $4,925 | $5,478 | $5,693 | $20,946 | 5% | 17% |

| Hamilton | $3,937 | $4,092 | $4,595 | $4,757 | $17,381 | 4% | 21% |

| Windsor | $3,549 | $3,800 | $4,401 | $4,758 | $16,508 | 4% | 34% |

| Oshawa | $3,471 | $3,779 | $4,330 | $4,762 | $16,342 | 4% | 37% |

| London | $3,459 | $3,665 | $4,396 | $4,673 | $16,193 | 4% | 35% |

| Ottawa | $3,113 | $3,202 | $3,889 | $4,197 | $14,401 | 3% | 35% |

Who pays the most in 2025 — and why?

Toronto households now spend on average close to $6,000 a year on combined auto and home insurance — the highest among the six cities. The main reason: claims in Toronto are both more frequent and more expensive.

Meanwhile, auto insurers haven’t been able to charge enough to cover rising losses.

Auto rate increases must be reviewed and approved by the Financial Services Regulatory Authority of Ontario (FSRAO), which can delay insurers’ ability to respond to rising costs.

When rate approvals lag actual loss trends, Daniel Ivans, Rates.ca insurance expert and licensed insurance broker says, “as market pressures intensify, they inevitably translate into noticeable rate spikes.”

Toronto and Hamilton also face structurally higher risks: they are major auto‑theft hot spots, have dense traffic that drives up collision and repair costs, and see growing water‑damage claims — now the leading cause of property losses, according to Statistics Canada. These factors push their premiums higher than in other cities.

Ottawa sits at the opposite end with a 3% insurance‑to‑income burden.

Read more: The 10 most stolen vehicles in Canada for 2025

Ontario insurance rates spike sharply from 2022–2025

Across all six cities, premiums rose steeply from 2022 to 2025, with the largest increases in Oshawa (+37%), London (+35%), Ottawa (+35%), and Windsor (+34%). Hamilton (+21%) and Toronto (+17%) saw slower but still significant growth.

Nationally, insurers have faced claims costs rising faster than the timing of rate filings. Statistics Canada reports that auto‑parts, maintenance, and repair costs increased by 22.3% from 2019 to 2024. Median new‑vehicle prices rose 61.5% and used vehicles 82.2%, leading to more expensive claims.

FSRA notes that persistent inflation in parts and labour, more advanced vehicle technology, and rising auto theft continue to pressure Ontario’s auto‑claims costs. Since insurers must apply to FSRA for any rate changes and support them with recent claims data, approvals can lag when cost pressures aren’t yet reflected in the historical data used in filings.

Across every city, 2024 delivered the steepest year‑over‑year premium increases. London saw auto premiums rise by up to 17% and home by 25%, while Windsor and Ottawa recorded auto increases above 18%.

Property insurance has faced even greater pressure. Canada recorded $8.5 billion in severe‑weather losses in 2024 — the highest ever, nearly triple 2023’s total and 12 times the early‑2000s annual average. Floods, hailstorms, wildfires, and extreme rainfall drove record payouts, with Ontario alone facing nearly a billion dollars in flooding. This surge in catastrophic events has reshaped home‑insurance pricing as insurers absorb higher and more volatile losses.

“The past 5 to 10 years have shown just how much home insurance exposure has intensified. The risks are very real, and the industry is feeling it," Ivans says.

Learn more: Is severe flooding making your home uninsurable?

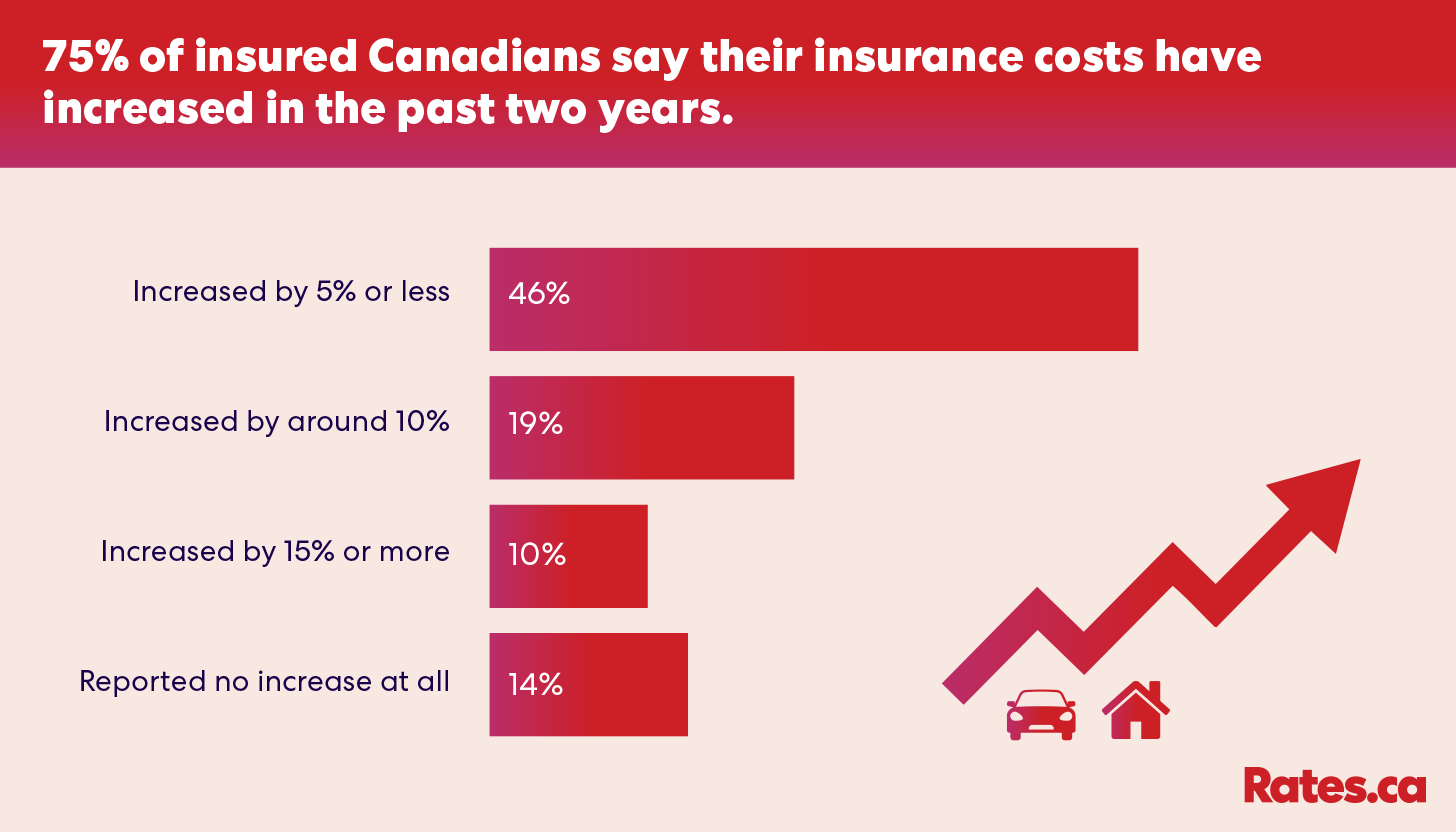

75% of insured Canadians say their premiums have increased over the past two years

The premium hikes haven’t gone unnoticed. According to the Leger survey commissioned by Rates.ca, three in four insured Canadians (75%) saw their insurance costs rise in the past two years.

Among those reporting increases:

- 46% saw hikes of around 5% or less

- 19% saw increases of around 10%

- 10% saw increases of 15% or more

- 14% reported no increase

- 11% said they don’t know

The more you own, the more you have to insure – and the more you pay.

Canadians 35+ — who are more likely to own both a car and a home — report experiencing increases at a higher rate (78%) than those 18–34 (64%). However, they are more likely to say the increase they’ve seen is around 5% or less.

However, higher-risk individuals are also susceptible to premium increases, says Ivans.

“For some new drivers, or for those with tickets or past claims, car insurance can run from $600 to $800 a month. That puts it in the same category as rent or groceries, or household expenses, and it’s a real strain for many consumers,” he says.

Related: 5 expenses that will cost Canadians more in 2026

Nearly two-thirds of insured Canadians are taking action to offset premium increases

Rising premiums are reshaping consumer behaviour. According to the survey, 63% of insured Canadians took steps to lower costs:

- 40% shopped around

- 30% asked for discounts

- 21% changed or removed parts of their coverage

- 3% upgraded their home or vehicle (7% of 18–34 vs. 2% of 35+)

The financial strain of insurance is already showing up in other ways. Auto affordability is also being directly affected at the point of purchase.

“High premiums deter buyers and can stop deals altogether. Particularly among newer or less experienced drivers, some are seeing insurance quotes that rival or even exceed their monthly vehicle finance payment, and in those cases, they’re choosing to walk away from the purchase entirely,” says Dan Park, CEO at Clutch Canada.

Related: Does your insurance cover the full replacement cost of your home?

Don’t cut coverage – find discounts instead

According to the survey, one in five insured Canadians are cutting coverage to save money. However, Ivans cautions that doing so might lead to bigger expenses down the road if something goes wrong.

“Reducing coverage increases your exposure,” he says. “You could find yourself having to spend a lot of money unexpectedly.”

Instead of cutting coverage, he urges households to focus on strategies that reduce premiums without sacrificing protection.

Discounts remain one of the most reliable ways to manage costs:

- Bundling home and auto: up to 20%

- Multi‑vehicle: up to 20%

- Usage‑based insurance (telematics): up to 30%

"By combining the quick savings that the multi-line, multi‑vehicle, and telematics discounts offer, households can meaningfully lower their premiums and regain significant control over rising costs,” says Ivans.

Lastly, he recommends shopping around for insurance.

“Insurance companies have peaks and valleys,” he says. “Find the company in a ‘valley.’”

Read next: Cheap(er) car insurance: Strategies to save money

Methodology

Leger is the largest Canadian-owned full-service market research firm. An online survey of 1,536 Canadians aged 18+ was completed between February 6th to 9th, 2026, using Leger’s online panel. Leger's online panel has approximately 500,000 members nationally and has a retention rate of 90 per cent. A probability sample of the same size would yield a margin of error of +/- 2.5 per cent, 19 times out of 20.

*When we refer to insured Canadians or insured households, these are Canadians who have at least one insurance policy on a home, apartment, condo, and/or vehicle.

Auto insurance quotes from Rates.ca reflect the lowest winning quotes for drivers aged 30 or older with a clean driving record, based on quotes for a single vehicle and a single driver. Home insurance quotes are derived from aggregated data across the Rates.ca Group Ltd. family of rate aggregators, calculated using the average of the top three winning quotes.

Save on Ontario auto insurance

Auto insurance rates change often, so how do you know if you're still getting the best deal? By comparing car insurance quotes upon renewal and at other key milestones (such as when you buy a new vehicle, or more to a different neighbourhood) you can make sure your rates remain competitive. Save money by comparing Ontario car insurance quotes today.

Arshi Hossain

Arshi Hossain, Associate editor

Arshi Hossain is the associate editor at Rates.ca. She has 4+ years of experience in delivering strategy-backed digital content through various mediums. Her expertise lies in breaking down complex information, meeting people where they are, and in the moments that matter.

Prior to joining Rates.ca, she worked in the editorial and digital content space at Wealthsimple, supported digital strategies, and UX writing for payment products and solutions at Bank of Montreal. She has also worked with startups to support editorial, content writing, communications, copywriting, and marketing needs.

Featured Topics

With only 13% of Canadians open to buying autonomous vehicles, experts expect adoption to begin through ride-hailing services before widespread ownership.

As extreme weather intensifies, resilient Canadian homes sell for more: upgrades can add up to 5.6% to resale prices, yet many listings don’t mention them.

After a sluggish 2025, EV interest in Canada is climbing again: searches are up 40%, and nearly one‑third of Canadians say they’re open to buying an electric vehicle.

In Toronto, auto insurance eats up 70% of total insurance costs, compared to 60% in Ottawa and 65% in Hamilton.

Despite recent interest rate cuts, 35% of Canadians now see condos as a poor investment, but they remain a key entry point for young and first-time buyers.

Are used cars always the cheaper choice? A closer look at the Ford F-150 and Toyota RAV4 shows how depreciation, insurance, and maintenance shape the true cost of ownership—and why the answer isn’t so simple.

Severe weather is driving up Ontario home insurance premiums, with water damage claims adding $376 and wind-hail $386 annually. Climate change, repair costs, and aging infrastructure deepen the strain on homeowners.

Nobody wins in a trade war - except, perhaps, car thieves.

Road rage remains a serious issue in Canada, with over half of drivers admitting to aggressive behavior—often fueled by stress, anonymity, and emotional disconnection behind the wheel.