Choose an Insurance Quote

Rates.ca Annual Best

Auto Insurance Study 2026

When it comes to auto insurance, customer satisfaction is more than just a buzzword — it's the foundation of success for insurers. The Rates.ca Annual Best Auto Insurance Study 2026 offers a comprehensive look at what matters most to policyholders by ranking insurers across several key performance categories. These categories represent a critical component of the customer experience and highlight the features that set the top insurers apart.

Here are the best auto insurance companies, according to consumers.

Annual Best Auto Insurance Study 2026

- Winners of the Best Auto Insurance Study

- Insights from the Rates.ca Annual Best Auto Insurance Study

- Most Trustworthy

- Best Auto Claims Experience

- Best Product & Value

- Best Communication & Clarity

- Claims satisfaction and real value: Where insurers deliver beyond price

- How top insurance companies are responding to lagging UBI adoption

- Methodology

Best Overall Insurance Company

For the third consecutive year, CAA Insurance Company has clinched the title of Best Overall Insurance Company, as well as ranking first for Most Trustworthy, Best Product & Value and Best Communications & Clarity.

Intact is also proving itself a mainstay, placing second in Best Overall insurance company for the second time as well as gaining distinction for their claims service and ease of reporting.

The best car insurance companies of 2026

Drivers should always compare multiple quotes to find the best policy for their needs, and that doesn’t always mean the lowest-priced premium. Instead, a great rate should provide value and quality, with attentive customer service, an easy claims process, and personalized policy offerings.

The Rates.ca Annual Best Auto Insurance Study surveyed 14,676 auto insurance customers in Ontario about their experiences with Canada’s top auto insurance providers. These customers are from five major insurance brokerages that collectively serve more than 220,000 personal line customers.

Customers were asked about their satisfaction levels across multiple categories, from claims processing to ease of communication, as well as coverage options and overall trustworthiness.

Here are the top-ranking auto insurance companies in 2026.

Rates.ca Annual Best Auto Insurance Study 2026

CAA Insurance Company

About the winner

CAA Insurance Company ranks as the top insurer for the third year in a row, also placing first in: Most Trustworthy, Best Product & Value, and Best Communication & Clarity.

Customers praise its low rates and strong claims service. Many use its recommended repair shops.

Its products address real needs, like MyPace, which rewards low-mileage drivers skeptical of traditional usage-based insurance.

Key takeaways

- CAA Insurance leads the market with strong customer satisfaction.

- Competitive rates are the top reason customers choose it.

- The company scores highly for product value, meeting customer needs, and policy innovation.

- It also excels in communication clarity, with nearly all respondents satisfied with their policy documents and over half reporting they are very satisfied.

Intact Insurance

About the winner

Intact Insurance achieved outstanding scores for its claims process. Customers find Intact reps easy to reach, knowledgeable, and proactive. The vast majority report quick claims resolutions.

Over half of customers bypassed their broker and went straight to Intact, underscoring its reputation for hassle-free service.

Of all insurers, Intact Insurance customers are also the most likely to use the company’s app for updates.

Key takeaways

- Intact Insurance is a trustworthy brand, according to the majority of customers surveyed.

- Top-ranked for ease of its claims process; customers say it’s clearly outlined and that reps are helpful.

- Quick claims handling drives satisfaction, with nearly two-thirds of those very satisfied.

- Intact Insurance customers are more likely to reach out directly than calling their broker.

Northbridge Insurance

About the winner

Northbridge Insurance promises quick support: calls are answered within 20 seconds, and an adjuster follows up within three hours.

This speed and efficiency helped drivers rank it among Canada’s best car insurers.

It earns strong marks for claims experience, and customers say it delivers solid value for the premiums they pay without compromising service.

Key takeaways

- Northbridge Insurance is a trustworthy brand according to survey respondents.

- Earned top marks for claims experience across virtually all aspects of the claims process

- Ease of claims handling and expert representatives are key strengths for Northbridge Insurance.

- High ratings for product offerings and overall value.

How we got our ranking

To properly evaluate how great an insurance company is, you have to look way beyond online reviews. In collaboration with Pollara Strategic Insights, we surveyed 14,676 drivers in Ontario about their interactions with their insurers and specific experiences when filing claims to capture new trends and evolving expectations.

According to our methodology, we also asked them to rate their satisfaction with their insurance companies across a few critical areas, including: brand trustworthiness, claims experience, communication, products and billing.

This year, we also expanded the field and allowed insurers to rank for the following titles:

- Best Overall

- Most Trustworthy

- Best Auto Claim Experience

- Best Product & Value

- Best Communication & Clarity

To find the best overall scores, we took the scores for each survey category and weighted averages based on customer demographics, brokerage and insurance carrier.

With claims back on track, how can consumers know which policy to pick? The answer isn’t always the lowest price

By Igal Mayer, CEO Rates.ca

Good claims service is the cornerstone of the insurance business.

And insurers struggled to deliver on that key service for years after the pandemic threw a wrench in the workings of global supply chains.

Disruptions meant simple repairs could take months to fix, and vehicle replacement times were stretched well beyond standard, leaving many drivers out of pocket for unexpected, costly expenses such as rental vehicles for extended periods of time.

Drivers unlucky enough to have had to make an auto insurance claim in Ontario during this time may have experienced a sub-par claims experience, but the results of the Rates.ca Annual Best Auto Insurance Study show that in 2025 the insurance industry has recovered, with satisfaction with claims service rising eight percentage points from 2023 to 81%.

Now that claims are back on track, consumers should look to how insurers are differentiating themselves to choose the right one for their needs. Even though many survey respondents understandably remain price-conscious this year — with 36% of respondents choosing their insurer because they offered the lowest price — the right coverage isn’t always the cheapest option. And as we saw during the pandemic and its aftermath, being caught without the coverage you need can be an expensive mistake.

Not all insurers will offer the same things, especially when it comes to digital methods of communication. For Gen Z consumers, insurers investing in apps, online portals and website capabilities for making claims and conducting business may offer better value.

According to the study there is, unsurprisingly, a trend away from phone calls for making claims among Gen Z respondents and a corresponding uptick in the use of digital tools. While the majority still prefer using the phone when making a claim, that number drops significantly with age, with about 60% of Gen Z, just under 70% of Millennials calling in to start a claim, compared with 80% of Boomers.

The insurance industry lags behind other comparable industries in implementing digital communications, so those that value the ability to type rather than call in a claim will need to shop around to find the right fit.

Innovative product offerings, such as usage-based insurance (UBI), will also differ from insurer to insurer. While the study shows increasing numbers of people are familiar with UBI, there hasn’t been a corresponding increase in adoption. It may be an image problem – as a digital offering that requires some set up, some may consider it an inconvenience. But according to the study, across all age groups, 96% of respondents who have UBI policies found it easy to set up, 71% agreed that it reflects their driving habits and 88% said they would likely continue with a UBI policy when they renew.

For consumers concerned with high premiums – and insurance premiums are likely to continue to rise throughout 2026, though not at the same pace as we’ve seen in the past few years – a UBI policy offers a way to keep premium costs in check while encouraging safer driving.

Auto insurance is mandatory, but who you choose as your insurer is not. Regularly reviewing policies before they renew and comparing offerings from different insurers can ensure that consumers have the right policy with the right insurer when they need it most.

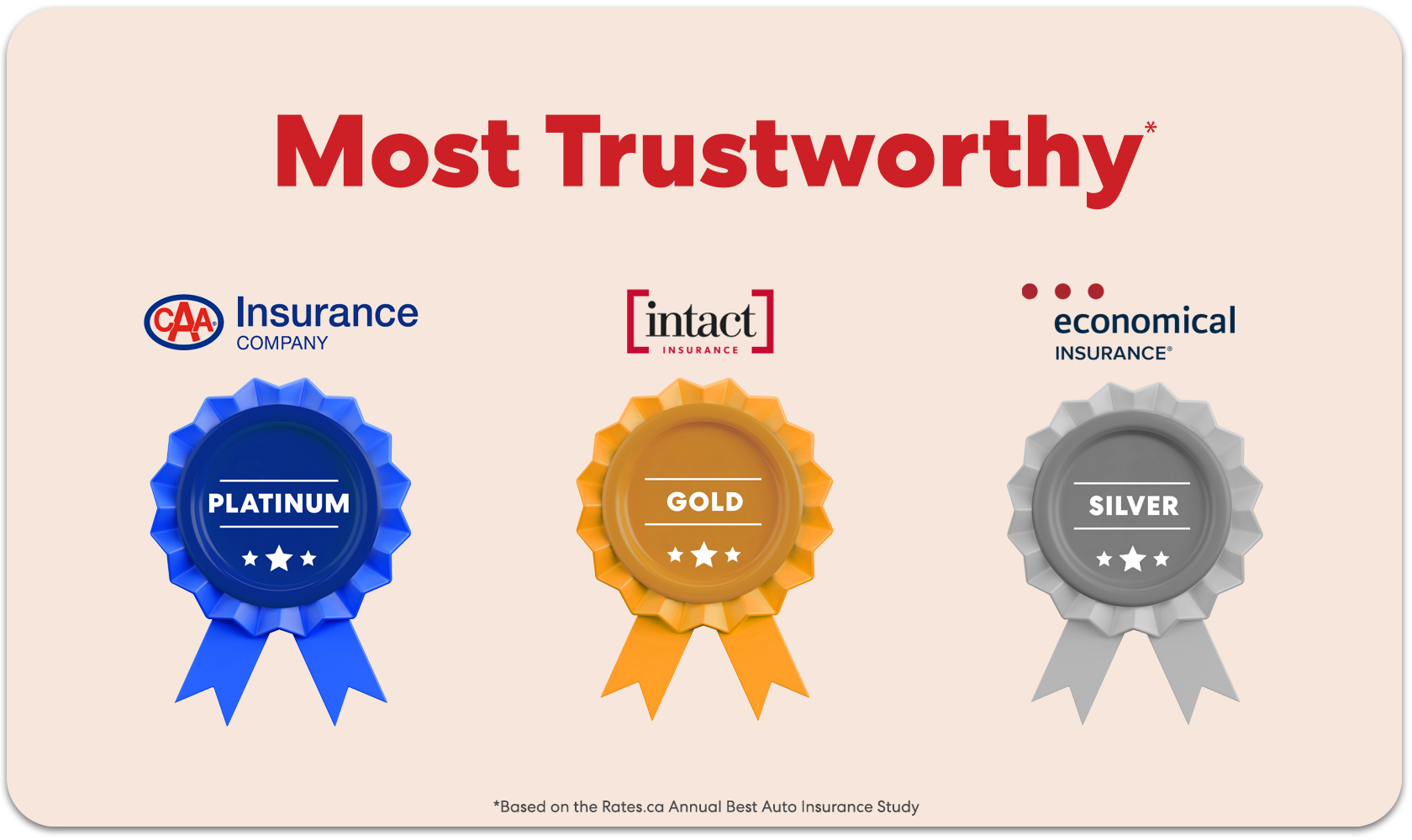

Most Trustworthy

The single biggest driver of consumer satisfaction is whether their insurance company is perceived as a trustworthy brand. Overall, 75% of customers believe that their insurer is a trustworthy brand, with 45% ranking their carrier as “Excellent” in this regard.

This year, CAA Insurance topped the list for the third year in the row, while Intact jumped one space up from last year. Economical Insurance, owned by Definity, made a major leap from last year, entering the leaderboard for the first time since the Study began.

Best Auto Claims Experience

As all drivers who have had to file a claim with their insurer know, claims experience can make or break your confidence and overall perception of the insurance company. On their part, insurers are constantly striving to optimize the process.

To come up with the top three insurance companies with the best auto claim experience, we evaluated customer satisfaction on key aspects of claims service, including timeliness and knowledgeable representatives.

This year, overall satisfaction with the claims process among those who filed an auto claim in the past year improved by eight percentage points to 81% from 2023 to 2025.

Best Product & Value

This year marks the introduction of a new category: Best Product & Value. As customers become more price-sensitive, insurers are focused on delivering good value for the premiums charged.

The top-ranking insurance companies in this category offer a diverse range of coverage options and innovative products that meet each driver’s personal needs, including ease of billing. CAA Insurance excelled at all elements of billing statements, from issuing easy-to-understand statements and communicating billing updates or changes, as well as offering multiple payment options to customers.

Best Communication & Clarity

Communication is the backbone of any healthy relationship, and the one between insurer and customer is no different.

This new category evaluates perceptions of and satisfaction with carriers’ communication assets, from policy documents to diversity of communication channels. The Study found that half of customers have contacted their insurance carrier directly over the past two years, with top reasons being to update coverage and billing payments. Most customers also used the phone to contact their carrier.

However, with increasing digital channels available, insurers have more reason to be innovative, fast, and attentive when communicating with their customers.

Claims satisfaction and real value: Where insurers deliver beyond price

Claim satisfaction is climbing even as price sensitivity intensifies.

The latest Rates.ca Annual Best Auto Insurance Study shows that 81% of claimants were satisfied with their claims experience in 2025, up eight percentage points since 2023. This comes at a time when consumers are increasingly focused on cost: 36% of respondents said they chose their insurer based on the lowest price, up from 34% in 2024.

Economic pressures are real. The Insurance Bureau of Canada reports that factors such as surging parts prices, rampant auto theft, and inflation, compounded by supply chain issues have driven insurance claims costs over the last few years. In Ontario alone, auto theft claims costs surged by 524% between 2018 and 2023, adding an estimated $130 to the average annual premium.

Rather than letting these pressures erode service quality, insurers have restored claims performance to pre-pandemic levels and beyond.

Overall satisfaction with carriers remains steady at 83%, but the real story is in claims: improvements in responsiveness, communication, and timeliness have helped insurers deliver value when it matters most.

Better customer experience adds value to the claims process

When a collision happens, saving a few dollars a month matters far less than having a claims process that works.

Among customers who filed a claim in the past year, overall satisfaction with claims service reached 81%, up from 74% in 2023 — a steady improvement that signals insurers are investing where it counts.

Customers who feel informed and receive quality service throughout the claims journey are more likely to perceive fair value beyond just price. Insurers that have high levels of claims satisfaction perform well on all aspects of claims service, including:

- Ease of reporting a claim

- Proactive communication throughout the claim

- Timeliness of resolution

“Ultimately, strong communication builds trust. Even price-sensitive customers feel more confident they’re being treated fairly and receiving helpful guidance, which makes the claims experience smoother and more reassuring,” says Craig Richardson, senior vice president and chief claims officer at Definity.

First notice of loss (FNOL) sets the standard for claims excellence

That first interaction, known as the first notice of loss (FNOL), is the moment that sets the tone for the entire claims journey.

Northbridge Insurance ranked first for the second year in a row in the Best Auto Claims Experience award category. Lynne Cool, vice president of claims at Northbridge, says speed and clarity are non-negotiable when it comes to claims management.

“We promptly answer phone calls when claims are reported — within 20 seconds every time — and our adjusters follow up within three hours of a claim being filed,” she says.

Northbridge consistently also ranks highly for claims satisfaction, outperforming in ease of reporting, clarity of process, and timely resolution.

While the majority (73%) of survey respondents used the phone to start a claim, younger respondents were more likely to use digital methods of communication such as email, app, website or online chat for both making a claim and receiving updates throughout the claims process.

“Clear communication and clarity help set realistic, transparent expectations from the very start of the claims process,” says Richardson. “Proactive updates throughout the claim also help prevent surprises, particularly around timing and costs.”

Insurers that rank highly in the study understand the importance of offering multiple communication channels for customers, especially during the claims process.

“Our broker-led model and direct adjuster access meet customer needs on their preferred channel,” says Mikael Honore, VP, Claims Operations, APD & Property for Gore Mutual Insurance, which earned top marks for Best Communication & Clarity and Best Product & Value. “Which research shows drives satisfaction and loyalty.”

In addition to meeting customers on their preferred communication channels, Gore also ensures that consumers understand what’s happening at every step of the claims process, which helps solve any burgeoning problems quickly and efficiently.

“Adjusters explain depreciation, matching and settlement calculations in plain language so brokers and customers can easily follow the logic,” says Honore. “Within defined guardrails, front-line teams resolve key issues on first contact.”

Why this defines real value

When insurers excel at responsiveness, communication, knowledge and quick and efficient claims resolution, customer satisfaction levels become high, even as price-sensitivity increases. Claims service is the ultimate test of value, and carriers are proving that strong processes and clear communication earn loyalty.

As Honore puts it: “We show customers we stand for more than just a transaction.”

How top insurance companies are responding to lagging UBI adoption

With economic uncertainty squeezing household budgets, usage‑based insurance (UBI) offers a way for drivers to cut premiums while promoting safer habits.

Yet despite the benefits, the Rates.ca Annual Best Auto Insurance Study shows that while familiarity with UBI continues to improve, there hasn’t been a corresponding increase in adoption.

UBI works through telematics. A smartphone app or an in‑vehicle device tracks kilometres driven and how people drive—things like acceleration, braking, and speed. Insurers then apply discounts based on actual driving behaviour, tying discounts to safe driving practices.

UBI awareness is up, but adoption still trails

Results from the Rates.ca Annual Best Auto Insurance Study 2026 show how familiarity with UBI compares to actual uptake. According to the study, two-thirds (66%) of drivers say they’re at least somewhat familiar with UBI, a five-point jump from last year.

Customers in Ontario who are most likely to be familiar with UBI are aged 30 to 39, women, and those who live in Toronto. Of all customers surveyed, 16% have a UBI policy. Among those who don’t, one in four (25%) would consider switching to receive a minimum 5% discount.

The study also shows that customers with a UBI policy are slightly more likely to rank their carrier as more trustworthy and report higher levels of satisfaction with their carrier.

With awareness climbing — and customers with UBI tend to perceive their carriers more favourably — how else are insurers working to get these programs into the hands of drivers who could benefit most?

The perception barrier

Chief underwriting officer of Gore Mutual Insurance Company, Chris Van Kooten, says the problem isn’t the product, it’s perception.

“Many drivers still see UBI as complicated—something that demands extra effort or exists to penalize,” Van Kooten says. “In reality, programs like ours are designed to be effortless, intuitive, and genuinely beneficial.”

The study shows that among those who’ve made the switch:

- 96% say enrollment was easy, including 65% who said it was "very easy"

- 79% call the product valuable to them personally

- 71% agreed that the discounts reflect their driving behaviour

- 88% said they would likely continue with a UBI policy when they renew.

“The real opportunity lies in reframing UBI: not as ‘monitoring,’ but as ‘empowering.’ It’s about demonstrating how safe driving habits are rewarded and how these programs deliver tangible value to customers,” says Van Kooten.

The importance of education

Both Gore Mutual and CAA Insurance Company say that if UBI is going to move beyond niche status, education has to lead the way.

“Education is central to adoption, and, as always, we begin with our trusted broker partnerships,” Van Kooten says.

Gore supports brokers and customers with FAQs, targeted communications, and a dedicated support line — tools that tackle misconceptions and show how UBI fits seamlessly into everyday driving.

CAA Insurance is taking a similar approach, focusing on transparency through direct conversations between agents or brokers and customers. To make those discussions more productive, the company created an Auto Insurance Guidebook to educate drivers on the basics of UBI and auto insurance in general.

“This resource allows drivers to have deeper, more productive conversations with their insurance agent or broker,” says Elliott Silverstein, Director of Government Relations with CAA Insurance.

In the Rates.ca Annual Best Auto Insurance Study for 2026, both Gore and CAA Insurance ranked among the top three insurers for offering products that meet customers’ needs and for clear, effective communication.

“We’re focused on making UBI easy for our broker partners to explain and simple for customers to understand,” says Van Kooten.

“As awareness grows, UBI becomes a natural choice for customers seeking personalization and lasting value,” he adds.

Why discounts alone are not enough as an incentive

Gore and CAA Insurance agree that price breaks help, but they’re just a starting point to encouraging UBI adoption.

To make UBI more appealing, Gore has added a gamified element to keep customers captivated.

Van Kooten notes that incentives “deliver the greatest impact when paired with engagement.”

For example, drivers can earn weekly rewards for exhibiting safe driving habits, redeemable for gift cards.

“Customers also receive a 10% discount upfront and can earn up to 20% at renewal, transforming insurance into an interactive experience that motivates safer behavior and reinforces long-term value,” says Van Kooten.

While these features reflect the traditional, behavior‑based approach to UBI, CAA Insurance uses the technology differently by aligning incentives with how much you drive rather than how well you drive.

In contrast, CAA Insurance focuses on personalization to incentivize customers.

“One size does not fit all when it comes to auto insurance,” says Silverstein. “We recognize that low-mileage drivers want to pay only for the coverage they actually need.”

This focus on tailoring coverage for low‑mileage drivers led to the 2018 launch of CAA MyPace, which Silverstein calls “a premier example of this shift.”

The program “allows low-mileage drivers to pay a Base Rate and then monitor their usage, paying only for the insurance based on the kilometers they drive,” he says.

So, for example, if you drive 6,000 kilometres, you could save up to 25% with CAA MyPace’s payment program.

Silverstein explains that this model allows consumers to reduce their insurance costs without changing their driving habits.

“Ultimately, customers who enroll benefit from lower premiums because they are driving less and, as a result, are involved in fewer collisions,” says Silverstein.

The road ahead

To get UBI into the hands of drivers who stand to benefit most, insurers are focusing on education, engagement, and reframing UBI as a tool for empowerment — not surveillance.

By simplifying enrollment, addressing misconceptions, and introducing unique perks and pay-as-you-go flexibility, they aim to make UBI a natural choice for drivers seeking personalization and lasting value.

How we came up with the Rates.ca Annual Best Auto Insurance Study

Rates.ca Annual Best Auto Insurance Study

The Rates.ca Annual Best Auto Insurance Study is the largest survey of auto insurance customers in Canada, contacting customers from five leading insurance brokerages serving more than 220,000 personal line insurance customers across Ontario, the largest market for private auto insurance in the country. Conducted by Pollara Strategic Insights, the survey was completed from August 25 to September 23, 2025, using an online survey methodology, surveying a total of n=14,676 auto insurance customers in Ontario who take part in decisions regarding insurance for their household. This is a survey dedicated solely to satisfaction with auto insurance, with questions focused on the entirety of experience with one insurance company to understand and measure what drives customer satisfaction. Underwriting carriers were identified by policy, not customer recall, ensuring accuracy in carrier identification. The study includes brands which are not typically reported in surveys of the general population of insurance consumers due to their relatively small market share.

About Pollara Strategic Insights

Founded in 1985, Pollara Strategic Insights is a Canadian public opinion and market research firm that provides custom quantitative and qualitative research as well as a suite of proprietary research models and syndicated studies. Pollara Strategic Insights is a founding, accredited Gold Seal member of the Canadian Research Insights Council (CRIC). They are in full compliance with the CRIC Canadian Code of Market, Opinion, and Social Research and Data Analytics, the CRIC Public Opinion Research Standards and Disclosure Requirements, the CRIC Pledge to Canadians and ISO 20252:2019.

For media inquiries, please contact:

Laura Fitch

Director of Editorial and PR

Rates.ca

lfitch@rates.ca

For inquiries about methodology, please contact:

Craig Worden

President & Chief Innovation Officer

Pollara Strategic Insights

CraigWorden@pollara.com

Latest auto insurance articles:

Learn how car financing works in Canada, what lenders consider, how credit scores affect rates, and how auto loan fraud may influence borrowing costs.

Used cars are still cheaper, but lower financing rates, warranties, and EV incentives are making new vehicles a stronger value proposition in 2026.

Learn how no-fault insurance works in Ontario and how drivers are impacted by July 2026 changes to accident benefits.

Having comprehensive-only insurance is necessary for stored vehicles in Canada that still face risks of theft, fire, flooding, and vandalism.

Car‑sharing services in Canada provide insurance, but coverage limits, deductibles, and exclusions can vary widely between providers.

How to reduce risk of your car getting caught in an underground parking garage flood and details on your insurance coverage options.