Choose an Insurance Quote

One home insurance claim could up your premium by 20%, says Rates.ca report

KEY FINDINGS

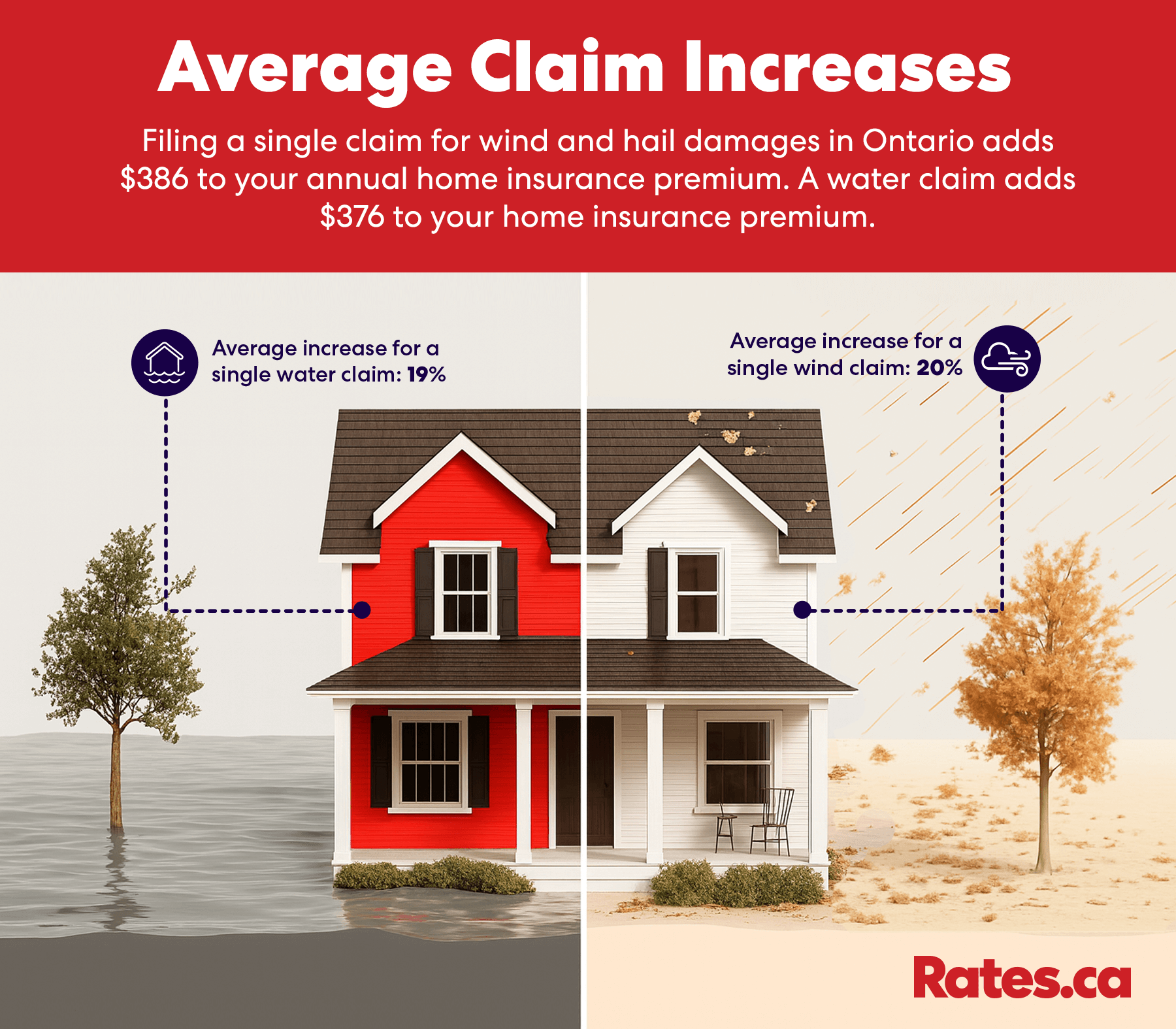

- A single water damage claim increases home insurance premiums by an average of $376 annually (19%) in Ontario, while wind-hail claims add $386 annually.

- Repairing a flooded basement costs at least $43,000 out of pocket, with weather-related repair costs surging 485% since 2019.

- Canada has seen a 115% increase in personal property damage claims since 2019.

- Mississauga ranks as the 6th most expensive city for home insurance in the GTA, with areas like Port Credit and Cooksville bearing much of the risk.

- Only 55% of Canadians carry overland flood coverage. For every dollar paid in insured flood losses, households face two dollars in uninsured costs.

While disasters like wildfires, floods, and storms dominate headlines, the hidden costs homeowners face after the skies clear are just as fearsome.

According to data from the Rates.ca insurance quoter, a single water damage claim can increase a homeowner’s home insurance premiums by an estimated $376 annually—or 19% of their overall premiums—in Ontario.

This report draws on insurance quoter data from the Rates.ca Home Insuramap, which uses weighted estimated averages from real home insurance quotes across cities and towns in Ontario. Specifically, it examines how much water and wind-hail claims add to annual premiums.

For those without specified coverage for insured perils like overland flooding, the financial stakes are even steeper. Repairing a basement after flooding can cost at least $43,000 out of pocket— a figure from 2019 that has likely ballooned in recent years. Since then, the cost of repairing weather-damaged property in Canada has surged by 485%.

Due to rising premiums to severe weather, the cost of protecting your home is climbing faster than ever. Here’s why.

Wildfires burn over 30 million hectares — over the size of New Brunswick — in just three years

Canada is warming at nearly twice the global average, and the consequences are clear: longer fire seasons, more intense droughts, extreme rainfall, and severe heatwaves. In just three years, over 30 million hectares of land have burned in wildfires—an area larger than New Brunswick.

“Over the past five years, Canada has experienced the three worst wildfire seasons on record, as well as major flooding, hail, and storm events,” says Dr. Anabela Bonada, managing director of climate science and operations at the Intact Centre on Climate Adaptation.

She says that compared to previous decades, the number of catastrophic weather events has increased significantly, and “their financial impact has quadrupled on average.”

For experts like Dr. Bonada, there’s no question: Climate change is the driving force behind these severe weather changes. In fact, she says that attribution studies found that the 2023 Quebec wildfires were made seven times more likely due to climate change.

When weather becomes expensive, so do your home insurance premiums

We can't control the weather, but homeowners are paying dearly for its consequences.

Based on quoter data, a single wind-hail claim adds an average of $386 to the annual home insurance premium for a 2,500-square-foot home in Ontario, while a water claim increases it by $376.

Every year since 2020 has ranked in the top ten worst years for insured losses from extreme weather. Since 2019, Canada has seen a staggering 115% increase in personal property damage claims and a 485% spike in the costs of repairing and replacing weather-damaged property.

According to Alex Walker, program manager of climate finance at Environmental Defence Canada, insurance premiums have grown at a pace far above overall inflation.

“Since 2020, the home and mortgage insurance component of the Consumer Price Index (CPI) has increased by 27.36%, compared to 15.38% for overall inflation,” they say.

While the replacement costs ballooned during the global pandemic due to supply chain disruptions and higher construction expenses, Walker says that premiums have outpaced even these increases, adding, “this suggests that extreme weather has been a decisive factor in driving up insurance costs for homeowners.”

Read more: Does your insurance cover the full replacement cost of your home?

Flood damage drives up home insurance costs across southern Ontario cities like Mississauga

Flooding has become the most damaging natural hazard in Canada, with water-related damage causing average annual losses of about $800 million over the last decade.

Overland flooding—when water enters homes through doors, windows, or cracks in the foundation— “is the single most common and costly natural disaster in Canada,” Walker says. Despite this, they noted only about 55% of Canadians carry overland flood coverage.

“Floods, historically considered 1-in-100-year events are happening with increasing frequency, driven by more intense rainfall events,” says Dr. Bonada.

As damage from these flooding events worsen, so do home insurance premiums across Ontario. Cities in the southern part of the province are seeing the steepest increases.

Mississauga: A case study in rising costs

Mississauga, one of the largest cities in the Greater Toronto Area (GTA), exemplifies how these factors converge to drive up home insurance costs, ranking as the 6th most expensive city for home insurance in the region.

Daniel Ivans, insurance broker and Rates.ca expert, highlights that Mississauga has several waterfront communities near Lake Ontario and flood-prone waterways.

And where you live within the city may change your insurance risks.

Spatial analysis revealed repeated flooding is particularly concerning in low-lying areas and neighborhoods with older infrastructure.

- High-risk areas: Port Credit, Cooksville, Lakeview, and Clarkson.

- Moderate-risk areas: Erin Mills and Meadowvale.

- Low-risk areas: Lisgar and Churchill Meadows, where modern construction and better elevation mitigate flood impacts.

“Add to all this, an aging infrastructure, and higher repair costs,” says Ivans, “and it makes Mississauga more vulnerable and more expensive to fix.”

Severe weather has plagued Mississauga for years.

In February 2012, Lisgar residents filed a $200-million class action lawsuit against the City, Region of Peel, Halton Regional Conservation Authority, and Ontario’s Environment Ministry, citing years of flooding that damaged homes and reduced property values. The lawsuit was eventually dropped in 2015.

More recently, the city has faced multiple record-breaking flooding events with devastating impacts on homes and infrastructure.

In the summer of 2024 alone, two “once-in-a-century” storms struck the region:

- July 16, 2024: 106 millimeters of rain fell in just a few hours.

- August 17-18, 2024: Up to 170 millimeters drenched parts of Mississauga and the GTA.

2025 home insurance cost in Mississauga vs. the GTA

| Rank | City | Avg insurance premium | Difference from Mississauga ($) | Difference from Mississauga (%) |

|---|---|---|---|---|

1 | Woodbridge | $1,032 | - $438 | -29.80% |

2 | Ajax | $1,134 | - $336 | -22.86% |

3 | Markham | $1,215 | - $255 | -17.35% |

4 | Milton | $1,221 | - $249 | -16.95% |

5 | Whitby | $1,280 | - $190 | -12.93% |

6 | Vaughan | $1,336 | - $134 | -9.12% |

7 | Oakville | $1,343 | - $127 | -8.64% |

8 | Aurora | $1,345 | - $125 | -8.50% |

9 | Brampton | $1,352 | - $118 | -8.03% |

10 | Pickering | $1,361 | - $109 | -7.41% |

11 | North York | $1,364 | - $106 | -7.21% |

12 | Uxbridge | $1,370 | - $100 | -6.80% |

13 | Oshawa | $1,372 | - $98 | -6.67% |

14 | Richmond Hill | $1,375 | - $95 | -6.46% |

15 | Caledon | $1,376 | - $94 | -6.39% |

16 | Newmarket | $1,406 | - $64 | -4.35% |

17 | Whitchurch-Stouffville | $1,412 | - $58 | -3.95% |

18 | Halton Hills | $1,414 | - $56 | -3.81% |

19 | Burlington | $1,430 | - $40 | -2.72% |

20 | Mississauga | $1,470 | $0 | 0.00% |

21 | East Gwillimbury | $1,482 | + $12 | +0.82% |

22 | King City | $1,504 | + $34 | +2.31% |

23 | Toronto | $1,523 | + $53 | +3.61% |

24 | Port Perry | $1,567 | + $97 | +6.60% |

25 | Georgina | $1,643 | + $173 | +11.77% |

26 | Etobicoke | $1,675 | + $205 | +13.95% |

Estimated 2025 average premium in Ontario: $1,565

According to Walker, labour shortages are more pronounced outside major cities, leading to longer repair timelines and higher costs for skilled trades (more on this below). Additionally, material costs are inflated in remote areas due to expensive transportation and limited supply chains.

As a result, they say, “post-disaster recovery [is] slower and costlier for homeowners in outside urban centers.”

Water vs. Wind-hail claims: How are they priced?

Insurance premiums aren’t directly impacted by the type of claim—whether for water or wind-hail damage—says insurance expert Ivans.

Data from quoter shows that the difference between the two is quite minimal: a single wind-hail claim leads to an average premium increase 1% higher than that of a single water claim.

According to Ivans, on a large scale, the real financial impact comes from losing your "claims-free discount" and potential surcharges. He says that filing one claim makes you statistically more likely to file another, which influences how insurers price your risk.

It isn’t just the affected homeowner who has to pay for weather damage. Hypothetically, says Ivans, if Mississauga’s weather-related claims doubled to $100 million in damages in a year, every policyholder’s premium would be indirectly affected, regardless of whether they made a claim or not.

Learn more: Rebates for climate-friendly changes to your home

Why are claims so expensive? The supply and demand squeeze

When severe weather strikes, a sudden surge in demand opens up for repairs, materials, and services, overwhelming supply chains and driving up costs in high-risk areas.

Take for example, the 2021 heatwave in British Columbia, which tragically resulted in 576 heat-related deaths between June 25 and July 1.

Simon Bernath, founder and CEO of FurnacePrices.ca, an online network of vetted HVAC contractors, observed a 200-300% spike in demand for air conditioning systems during this time.

“Because ACs were less common in the region, many people were unprepared,” Bernath says, adding that this lack of preparation likely contributed to the high number of deaths among vulnerable populations.

Materials to fix your home cost more than ever

Over the past decade, the cost of building single-detached homes has risen by 49.5%, driven largely by softwood lumber prices, which more than tripled between June 2020 and May 2021.

Other materials have followed suit. Steel, drywall, and basic supplies like pipes have seen sharp increases. In the second quarter of 2025 alone, plumbing materials rose 3.7%, while HVAC supplies increased 3%.

“Some of our partner contractors have seen a slightly higher increase in unit costs for the brands they sell—roughly 5% compared to the typical average increase of maybe 3%,” says Bernath.

He adds that parts costs have surged by as much as 20% year-over-year, with unit costs for many brands climbing as high as 8%.

Overall, since February 2020, the following materials have seen price increases:

- Cement, glass and other non-metallic materials: 36.6%

- Plastic and rubber products: 26.9%

- Logs, pulpwood, natural rubber, and other forestry products: 25.9%

- Fabricated metal products and construction materials: 41.3%

- Machinery and equipment: 21.8%

Tariffs will soon add another layer of extra costs — if they haven’t already

Canada imports billions in tariff-impacted materials annually, including $3.5 billion in glass, $3.1 billion in major appliances, $2.2 billion in hardware, and $1 billion in ceramic tiles. These tariffs ripple through the supply chain, forcing contractors to pass higher costs onto homeowners.

For example, repairing a broken furnace requires steel, aluminum, and electronic components—all materials subject to tariffs. Heat pump replacements and essentials like windows, doors, and carpeting have also seen steep price hikes.

Contractors are adapting where possible. Ryan Meagher, business development and lead estimator at BVM Contracting, says, “demand is off because of all the tariff talk.” He adds that his team is engineering steel out of projects to save clients money.

However, not all materials can be easily substituted. Since tariffs took effect in 2025, Statistics Canada reports that builders nationwide are experiencing higher costs and greater uncertainty, especially for essentials like steel and lumber. This has made managing project budgets more challenging.

Here’s how tariffs would affect different home repairs.

| Repair material | Key tariff-affected repairs |

|---|---|

| Steel and metal products | Beams, steel studs, and railings |

| Aluminum products | Windows, patio doors, garage doors |

| Appliances | Kitchen and laundry appliances, HVAC systems |

| Lumber and wood products | Framing, plywood, decking materials |

| Plumbing fixtures | Faucets, sinks, and tubs |

| Electrical components | Pot lights, panels, wiring |

| Flooring materials | Vinyl floors, engineered hardwood, ceramic and porcelain tiles |

Source: Renotec Canada

Labour shortages persist

Many partner contractors working with Bernath report significant challenges in finding qualified labor. This is an industry-wide trend. With 75% of homes over 20 years old and nearly five million needing repairs, the demand for qualified tradespeople far outweighs supply.

The construction industry faces a growing skills gap as over 30% of its workforce approaches retirement. Between 25,000 and 28,000 workers are expected to retire annually until 2033, while the industry needs to add 88,400 workers in the same period to meet rising demands.

Bernath says this issue is compounded by the seasonal nature of trades like HVAC, where demand fluctuates. It doesn't get any better during unusual weather patterns. Contractors struggle to balance “keeping technicians on payroll during slower periods while meeting surging demand during peak seasons.”

Related: How will US tariffs affect your auto and home insurance?

High-risk areas are growing—can your insurance keep up?

Many Canadians have no idea what’s in their insurance policies, particularly when it comes to overland flooding, which is not typically covered under standard policies.

As high-risk areas expand due to changing climate conditions, the danger of being uninsured becomes increasingly severe.

A 2016 survey found that 65% of Canadians believed their home insurance covered overland flooding, even though this wasn’t the case. By 2021, only 55% of homeowners had actually purchased this coverage, leaving a significant portion of Canadians exposed to one of the country’s most costly risks.

Even for those with insurance, outdated policies can leave homeowners vulnerable. “Rising costs for materials, labor, and equipment mean that even well-insured homeowners could face unexpected out-of-pocket expenses if their policies aren’t updated to reflect current market conditions,” explains Environmental Defence Canada’s Alex Walker.

The situation is further complicated as insurers refine their risk assessments. In some high-risk areas, coverage options are being reduced—or withdrawn entirely—leaving homeowners fully exposed to financial losses.

Dr. Bonada warns that new high-risk areas across Canada are emerging and will continue to do so as climate conditions evolve.

Insurance doesn’t just protect the structure of your home—it safeguards your belongings, covers temporary living expenses, and provides financial stability after a disaster.

Yet, the financial burden of flooding remains heavily skewed. For every dollar paid out in insured flood losses, households face two dollars in uninsured costs.

As Walker puts it, “the majority of the financial burden from flooding falls directly on homeowners rather than insurers.”

Don’t wait for disaster to strike. While filing a claim may increase your premiums, the cost of repairing your home out-of-pocket is far greater. Take the time to review your policy, update your coverage, and ensure you’re protected against the growing risks of climate-related disasters. In an era of increasing uncertainty, being proactive is the best way to safeguard your home, your finances, and your peace of mind.

Read next: How to prepare your home for Autumn

Methodology

Rates.ca’s quoter data shows how their home insurance rates compare to other parts of their city or province. The estimated premiums for each Forward Sortation Area (FSA) are based on the average of the lowest three quoted premiums. The premiums were acquired using a profile of a 45-year-old homeowner, who has been insured for at least 10 years and lives in a 2,500 sq ft detached house, built 40 years ago, with brick veneer, wood frame construction, natural gas heat, a 10-year-old roof and replacement cost of $500,000.

Don't waste time calling around for home insurance

Use Rates.ca to shop around and compare multiple quotes at the same time.

Finding the best home insurance coverage has never been so easy!

Arshi Hossain

Arshi Hossain, Associate editor

Arshi Hossain is the associate editor at Rates.ca. She has 4+ years of experience in delivering strategy-backed digital content through various mediums. Her expertise lies in breaking down complex information, meeting people where they are, and in the moments that matter.

Prior to joining Rates.ca, she worked in the editorial and digital content space at Wealthsimple, supported digital strategies, and UX writing for payment products and solutions at Bank of Montreal. She has also worked with startups to support editorial, content writing, communications, copywriting, and marketing needs.

Featured Topics

As the real estate market fluctuates, doing minor, strategic renovations may help improve your home equity and offset falling home values.

A comprehensive home insurance policy can help you cover significant repair costs from a water-damaged basement.

How to reduce risk of your car getting caught in an underground parking garage flood and details on your insurance coverage options.

Consider short-term home insurance additional options before you rent out your home to FIFA World Cup 2026 soccer fans.

Spring landscaping can affect your insurance. Minor grading changes can send water toward foundations, raising flood risk.

A backwater valve is a gate mechanism added to your wastewater outflow pipe that prevents city sewage from flowing back into your home.

As extreme weather intensifies, resilient Canadian homes sell for more: upgrades can add up to 5.6% to resale prices, yet many listings don’t mention them.

A weeping tile drainage system can help prevent water damage to your basement and property foundation.

Rebates available in Canada for improving resiliency and energy efficiency of your home can reduce future insurance claims.