Choose an Insurance Quote

Survey: Over half of Canadians not confident we’ll avoid a recession in 2025

With inflation tapering down and two consecutive rate cuts in June and July, it might seem that financial relief is on the horizon. However, most Canadians remain skeptical of this notion.

Refat Wohab, a 22-year-old computer programming student, is currently pivoting from a career as a pharmacy assistant. She says that although she has had her current job for three years, her role has offered little to no growth, especially when it comes to a pay raise.

“With the last few years being so awful – economy-wise, things just have to look up because my hands feel tied,” she says.

Maybe they will, maybe they won’t.

A recent Leger survey conducted on behalf of Rates.ca reveals a more realistic and less idealistic perspective, highlighting the prevailing pessimistic sentiments surrounding the economy.

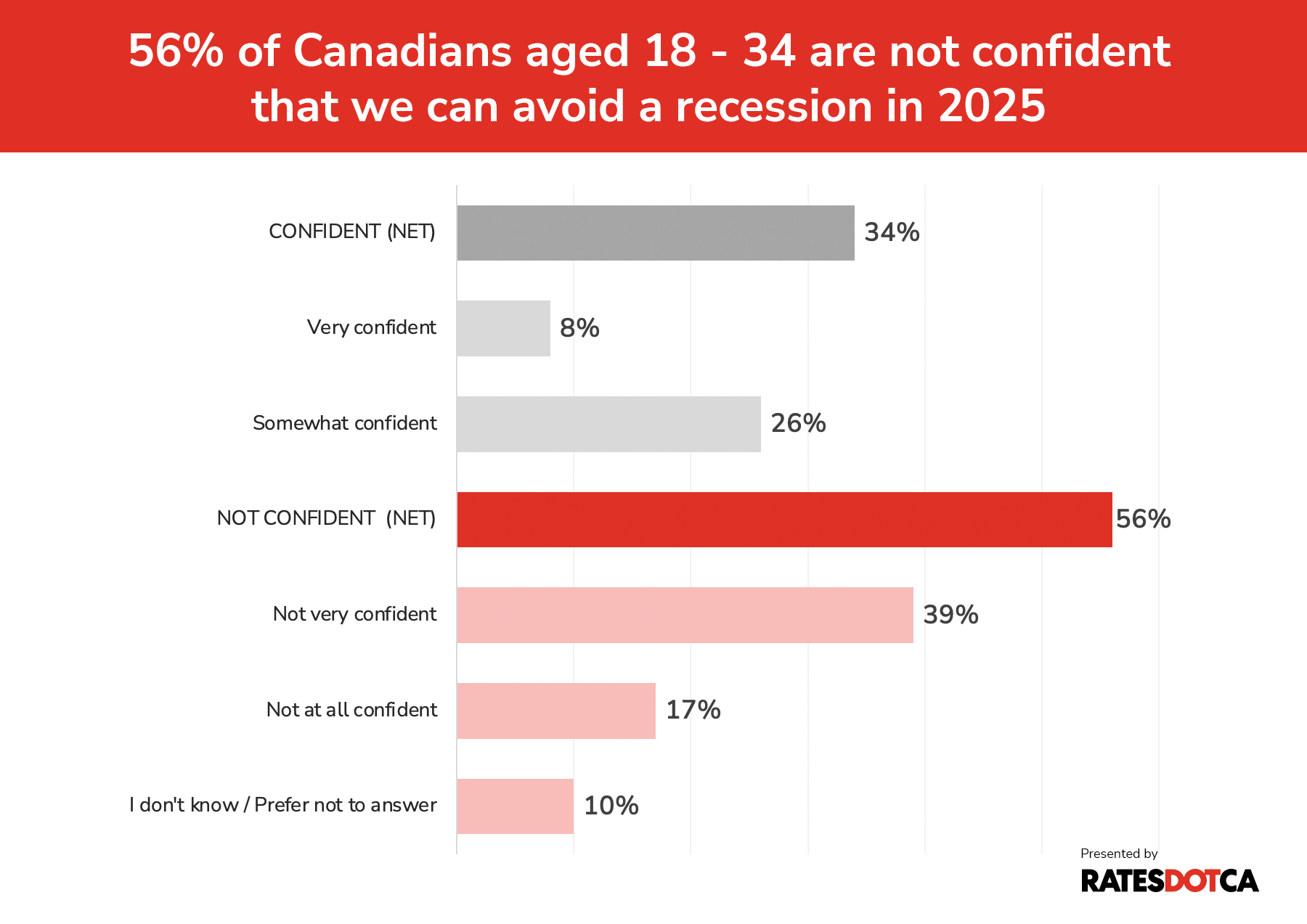

Canadians’ confidence about avoiding a recession: 51% of respondents have none

While Canada narrowly dodged a recession during the pandemic, just over half of Canadians are waiting for the other shoe to drop in 2025.

Only 5% of those surveyed are ‘very confident’ that Canada will hold off sinking into a recession, whereas 16% are ‘not at all confident’. This disparity highlights a pervasive sense of economic uncertainty among Canadians.

For many, incomes are not keeping up with inflation. The high cost of living and increasing interest rates have reduced disposable incomes, leading to financial strain. This situation forces people to make tough decisions about how to allocate their money.

“Over the past year, while the economy has grown largely thanks to population growth, on a per capita basis, consumer spending has fallen,” notes Tu Nguyen, an economist and ESG director at RSM Canada.

She adds that if consumer behavior of restricting spending persists, it could trigger a recession. But the good news is as long as the Bank of Canada continues to cut rates, some households may soon see relief from lower borrowing costs, businesses will resume hiring, and recession odds will be tapered.

What would a recession mean for Canadians?

During a recession, economic activity shrinks instead of growing. A recession is a period of economic decline that lasts for at least six months, characterized by a decrease in the gross domestic product (GDP), which is the total value of goods and services produced by a country.

However, you don’t have to be in a recession to adopt a “recession mindset,” which leads to a more cautious approach to spending and financial planning. This mindset is driven by several factors, such as:

- Economic uncertainty: High interest rates and inflation start to pinch at household finances, affecting Canadians’ spending power.

- Consumer behavior: People cut back on non-essential expenses, delay large purchases, and save more.

- Housing market: High mortgage renewal rates and borrowing costs make homeownership more expensive. Meanwhile, renters also feel the strain of higher rents and fewer options.

- Job market: While unemployment isn’t at crisis levels, job insecurity persists, influencing how people manage their finances.

Overall, this mindset leads to more conservative financial behaviors, impacting everything from retail sales to housing markets.

This behavior mirrors patterns seen during major recessions and financial crashes in history – think the Great Recession in 2008 or the pandemic, when inflation reached unprecedented heights, followed by a rapid increase in interest rates, which significantly reduced discretionary spending.

Are we in a recession, or does it just feel like it?

According to industry experts, Canada is not technically in a recession. There haven’t yet been two consecutive quarters of negative growth or the surge in unemployment.

And while Canada’s jobless rate stood at 6.4% in July, which is 1.5 percentage points higher than the record lows of two years ago, the economy has managed to stay afloat.

But whether or not we label it a recession, it can feel like one for many.

“While total household spending is being supported by strong immigration, per capita or per person spending has fallen for five of the past seven quarters,” says Olivia Cross, economist at Capital Economics.

So, while Canada is not in a recession right now, the economy is dragging along rather than outright contracting.

“The recent retail sales data echoes the message that individual consumers are spending more cautiously, with the weakness in sales volumes concentrated in discretionary sectors, such as clothing, accessories and electronics,” she adds.

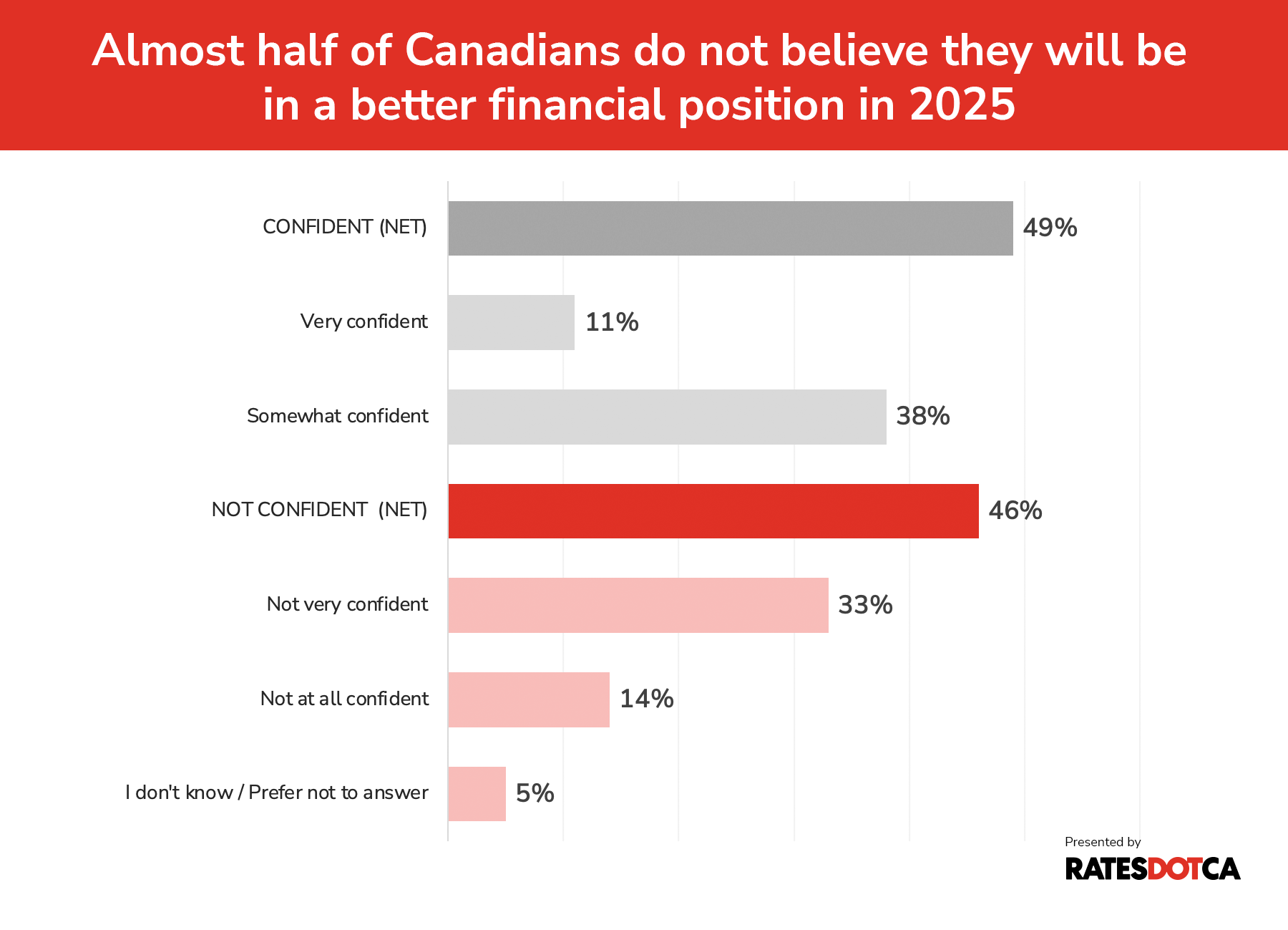

46% of Canadians doubt an improvement in their finances by 2025

According to Rates.ca’s survey, 49% of all respondents feel confident that they’ll be in a better financial position next year, and 46% reported not feeling confident.

Among the people most likely to be confident about their personal finances were young people between 18 and 34 years old. However, it is also this group that remains the most skeptical in the overall economy and Canada’s ability to avoid a recession.

“I have student loans that I’m paying for out of pocket, without financial help from parents, managing expenses like car insurance, whilst also balancing a social life and travel plans,” Wohab says. “I’ve been wanting to move out for a while, but with rising rent prices and low supply of units under rent control, the options are slim.”

Currently, young people are among the hardest hit by the weak job market. In July, the unemployment rate for youth aged 15 to 24 hit 14.2%, the highest it has been in nearly 12 years. For those who are employed, wage growth has also stagnated.

Older Canadians losing confidence in their ability to retire

With retirement becoming increasingly unaffordable and inching out of reach for many, the group least likely to feel confident about their financial prospects are people aged 55 and over.

Exactly half of respondents over the age of 55 reported feeling not confident about their financial futures. Like with young people, incomes for this age group have not grown with the general rate of inflation.

A report from Toronto Metropolitan University’s National Institute on aging reveals that only around one-third of those over 50 who intend to retire feel financially ready for retirement.

The top concerns for this group are the rising cost of living, running out of money, potential reductions in government benefits, and being able to afford major medical or long-term care expenses. Financial vulnerability is especially pronounced among those in fair or poor health and those with insufficient income.

“Some older Canadians are delaying retirement and choosing to work for longer to cope with higher costs of living,” says Nguyen. “Retirement income might not have kept up with inflation and rising cost of living, especially for those on fixed income”

Related: What should seniors know about mortgage renewals?

Who’s feeling good about next year? High earners and men

When asked how confident they were about their financial prospects in 2025, overall respondents were split nearly down the middle, with 49% of respondents saying they were confident and 46% stating otherwise.

Those confident about their finances in 2025 are more likely to be men (54% of men vs 45% of women), and people who earn more than $60,000 annually.

Perhaps unsurprisingly, the more income people earn, the more they are likely to be confident. Among those earning between $60,000 and $100,000, 53% felt confident about their finances. This confidence increased to 57% for individuals who earn more than $100,000.

On the flip side, 54% of respondents who earn under $60,000 say they are ‘not confident’. The less someone makes, the more likely they are to lack confidence in being better off in 2025.

Men are also more likely to be confident than women that Canada will avoid a recession (42% vs 30% of women). Meanwhile, 16% of women are also more likely to say they don’t know versus 10% of men.

The more homes someone owns, the less they’re likely to be concerned about the economy and their financial position - and vice versa

Over the past few years, many homeowners have been through the wringer of increasing mortgage payments and high inflation.

Despite the grim property landscape, however, homeowners – particularly owners of multiple homes – report feeling less concerned about the economy and their financial position than renters.

In fact, while just over half of all homeowners feel confident about their financial positions in 2025, owners of multiple homes, at 70%, are most likely to feel confident.

This comes even amidst a downturn in the condo market, an investment-heavy space where mortgage rates remain high even as property values have dropped, leaving far fewer buyers circling listings on the market.

However, Victor Tran, a mortgage broker and Rates.ca mortgage and real estate expert, explains that those who own multiple properties tend to be wealthier and are less affected by interest rate fluctuations due to their higher net worth and multiple income streams.

Meanwhile, other types of multiple-home owners, like people with vacation homes, are older, have small or no mortgages, and may have inherited properties, reducing their financial stress.

Instead, on the other end of the spectrum, it’s renters and people who don’t yet own homes (but plan to) who are least confident in their own finances and the overall economy.

Nguyen explains that while older homeowners have enjoyed the appreciation of their home values, renters face the challenge of rising rents, which makes it difficult to make ends meet.

She adds, “if homeowners sell, they enter the rental market where demand outstrips supply and vacancy is low, driving prices even higher while leaving people with few options.”

Renters account for the highest representation (21%) of those that said they are ‘not at all confident’ in their financial position in the next year.

Renters are most likely to be under the age of 35 (43%), earning less than $60,000 in annual income (49%), and living in urban areas (41%).

This group is also “dissaving” – meaning they’re spending more than they earn. Statistics Canada data from 2023 shows that renters spent nearly 9% more than their income, while homeowners managed to save 7% of their take-home pay. This reveals a significant financial gap between renters and homeowners.

Since the late 1990s, both renters and homeowners have seen their incomes rise at the same rate. However, the percentage of income that renters spend on housing has increased quickly.

“Both rent and mortgage interest payments have increased at a pace far above headline inflation and wage growth. While prices of other essential categories, such as gas and food, have moderated, housing costs are certainly outpacing income,” says Nguyen.

In 1999, renters spent about 25% of their take-home pay on housing, while homeowners spent 23%. As of 2022, the gap has only widened, with renters spending 29% of their income on housing, compared to 21% for homeowners.

Read more: Mortgage rates are creeping closer to 4% after the latest inflation news

Like many other younger adults, Refat Wohab is biding her time, saving money by living at home and focusing on her career. After all, in her 22 years on earth, she’s used to worse and has managed to cope.

“Gen Z is a generation that has faced a lot of adversity, what with being born post-9/11, living through the early 2000s recession, living through COVID-19, living through the emergence of technology,” she says. “The economy has gone down the gutter, and being alive is costly, and what sucks even more is growing up with little to no extra money.”

However, she continues to pick and choose how to define wealth in her life, by taking vacations when she can, putting items on credit when she needs to, and making the most out of an unfavourable economy.

“I'm at an age where I’m trying to build a life for myself but also help my parents with household expenses as their own means of income start to lessen,” she says. “It’s not just me. It’s my best friends, it’s my college peers, it’s my co-workers, it’s all of us having a hard time. But I mean, it can’t always be like this, can it?”

The answer? Well, it depends on who you ask.

Related: Then and now: How much more expensive is it to buy a home in 2024 vs. 1994?

Methodology

An online survey of 1,512 Canadians was completed between August 9 and 11, 2024, using Leger’s online panel. For comparative purposes, a probability sample of 1530 respondents yields a margin of error no greater than ±2.5%, (19 times out of 20). Results were weighted by gender, age, region, area, income, employment status, children in household, education, mother tongue, and ethnicity.

Compare Mortgage Rates

Engaging a mortgage broker before renewing can help you make a better decision. Mortgage brokers are an excellent source of information for deals specific to your area, contract terms, and their services require no out-of-pocket fees if you are well qualified.

Here at Rates.ca, we compare rates from the best Canadian mortgage brokers, major banks and dozens of smaller competitors.

Arshi Hossain

Arshi Hossain, Associate editor

Arshi Hossain is the associate editor at Rates.ca. She has 4+ years of experience in delivering strategy-backed digital content through various mediums. Her expertise lies in breaking down complex information, meeting people where they are, and in the moments that matter.

Prior to joining Rates.ca, she worked in the editorial and digital content space at Wealthsimple, supported digital strategies, and UX writing for payment products and solutions at Bank of Montreal. She has also worked with startups to support editorial, content writing, communications, copywriting, and marketing needs.

Featured Topics

With only 13% of Canadians open to buying autonomous vehicles, experts expect adoption to begin through ride-hailing services before widespread ownership.

As extreme weather intensifies, resilient Canadian homes sell for more: upgrades can add up to 5.6% to resale prices, yet many listings don’t mention them.

After a sluggish 2025, EV interest in Canada is climbing again: searches are up 40%, and nearly one‑third of Canadians say they’re open to buying an electric vehicle.

In Toronto, auto insurance eats up 70% of total insurance costs, compared to 60% in Ottawa and 65% in Hamilton.

Ontario households spent $14K–$21K on auto and home insurance in four years, city by city. 75% of insured households saw premium hikes in the past two years.

Despite recent interest rate cuts, 35% of Canadians now see condos as a poor investment, but they remain a key entry point for young and first-time buyers.

Are used cars always the cheaper choice? A closer look at the Ford F-150 and Toyota RAV4 shows how depreciation, insurance, and maintenance shape the true cost of ownership—and why the answer isn’t so simple.

Severe weather is driving up Ontario home insurance premiums, with water damage claims adding $376 and wind-hail $386 annually. Climate change, repair costs, and aging infrastructure deepen the strain on homeowners.

Nobody wins in a trade war - except, perhaps, car thieves.