Choose an Insurance Quote

Why Canadian housing seems unaffordable in 2026: A 35-year real estate disconnect

Ask the Expert is a monthly column where Steve Garganis, lead mortgage planner at Mortgage Architects and founder of CanadaMortgageNews.ca dives into what’s going on with mortgage rates and the Canadian housing market. Have a question for Steve on home buying and your mortgage? Reach out to us at media@rates.ca.

The dream of home ownership in Canada appears distant in today’s mathematical reality. Housing costs account for nearly 30% of household income. Older generations survived 12–18% interest rates in the 1980s and early 1990s. At the time, home prices equaled two or three years of household income. In today’s market, buying a home feels like embarking on a lifetime of debt.

How has Canadian housing affordability changed since 1990?

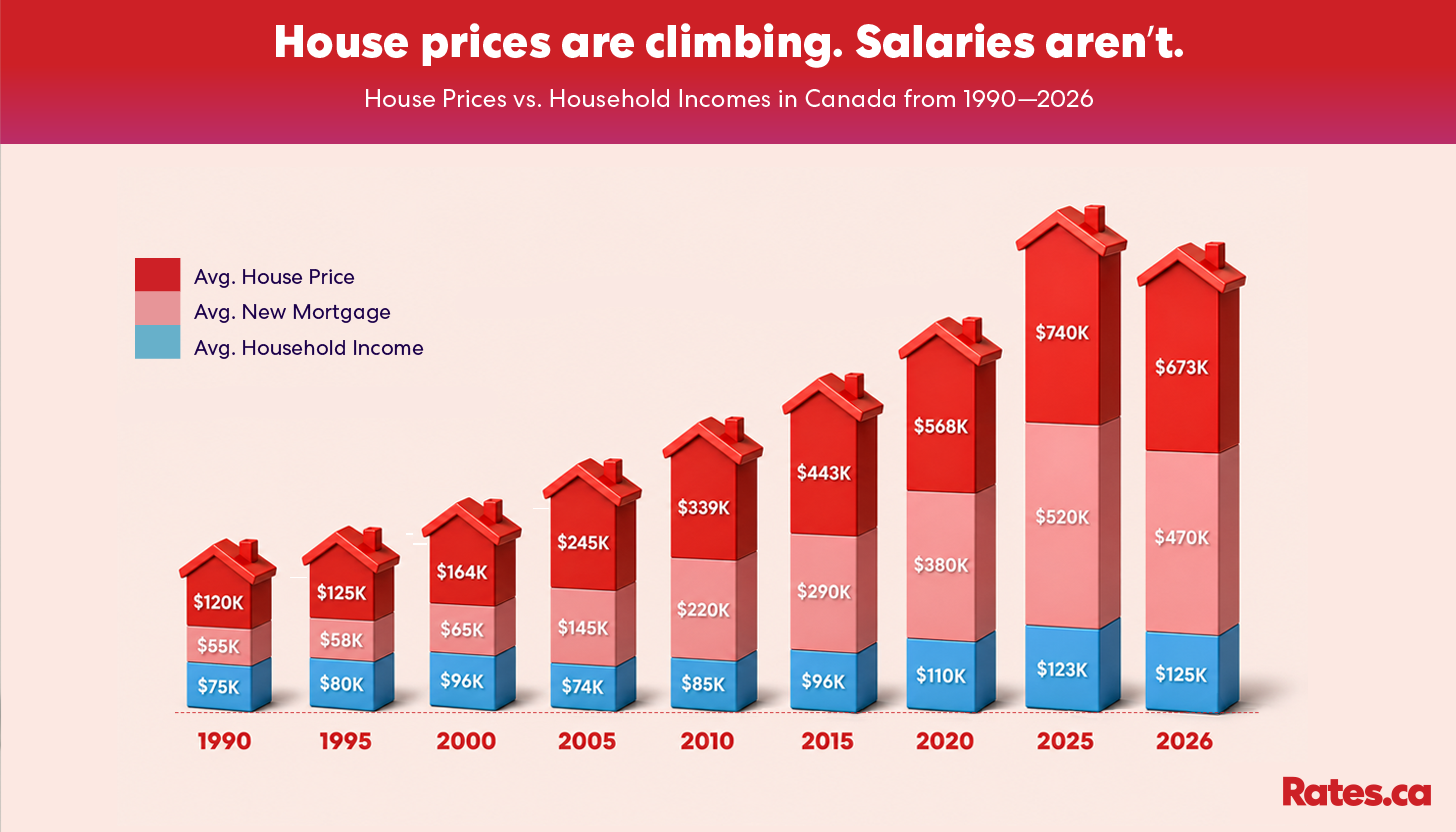

Canada's housing market has become more unaffordable over the years since 1990. Tracking average household income against exploding home prices from 1990–2026 provides a glimpse of stretched Canadian family budgets.

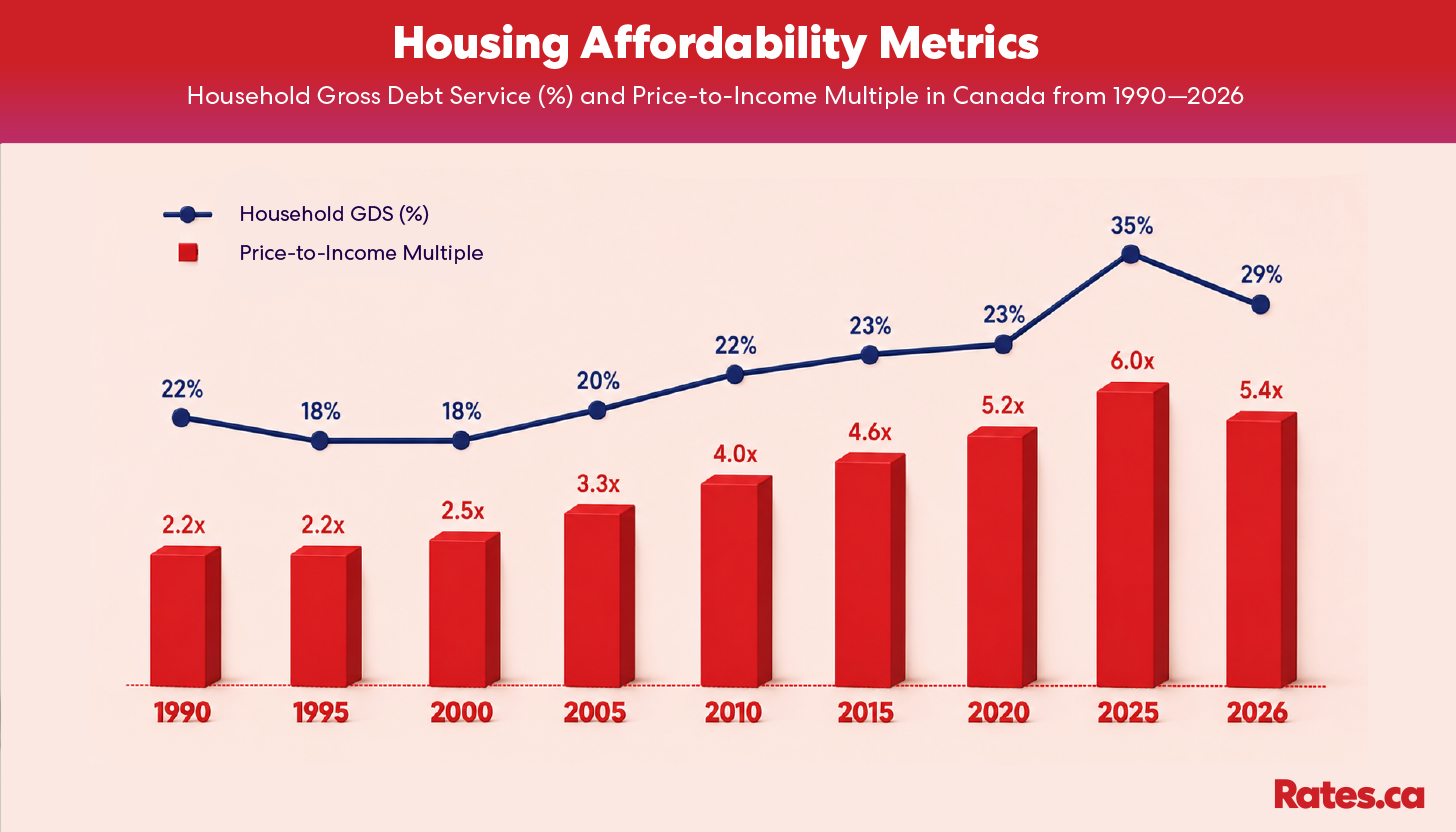

Annualized mortgage payments indicate exactly how much cash leaves a household every year just to keep a roof over their heads. Gross Debt Service (GDS) represents the percentage of your gross income required to cover housing costs. Lenders typically want to see a GDS no higher than 39%.

Canada Housing Affordability Key Metrics 1990–2026

| Year | Avg. House Price | Avg. Annual Household Income | Avg. New Mortgage Size | Avg. Rent (2-bedrm) | Avg. Mortgage Payment | Est. Household GDS | Price-to-Income Multiple |

|---|---|---|---|---|---|---|---|

| 1990 | $120,200 | $55,000 | $75,000 | $6,360/y | $9,300/y (~12% borrowing rate) | 22% | 2.2x |

| 1995 | $125,000 | $58,000 | $80,000 | $6,960/y | $7,620/y (~8.5% ) | 18% | 2.2x |

| 2000 | $164,000 | $65,000 | $96,000 | $8,160/y | $8,400/y (~7.5%) | 18% | 2.5x |

| 2005 | $245,000 | $74,000 | $145,000 | $9,000/y | $10,620/y (~5.5%) | 20% | 3.3x |

| 2010 | $339,000 | $85,000 | $220,000 | $10,320/y | $13,800/y (~4%) | 22% | 4.0x |

| 2015 | $443,000 | $96,000 | $290,000 | $11,520/y | $16,020/y (~2.75%) | 23% | 4.6x |

| 2020 | $568,000 | $110,000 | $380,000 | $13,980/y | $19,320/y (~2%) | 23% | 5.2x |

| 2025 | $740,000 | $123,000 | $520,000 | $18,600/y | $36,300/y (~5%) | 35% | 6.0x |

| 2026 | $673,000 | $125,000 | $470,000 | $19,200/y | $32,016/y (~4.75%) | 29% | 5.4x |

Source: Statistics Canada, Canadian Real Estate Association (CREA), Canada Mortgage and Housing Corporation (CMHC), Bank of Canada

Source: Statistics Canada, Canadian Real Estate Association (CREA), Canada Mortgage and Housing Corporation (CMHC). AI-generated infographic showing stacked 3D bars each with avg. house price, avg. new mortgage size, and avg. annual household income for each year from 1990 to 2026.

Snapshot of Canadian housing affordability 1990–2026

The erosion of Canadian housing affordability is undeniable. In 2000, a dual-income household used 18% of their gross income on housing. Even with recent cooling of the real estate market in 2026, GDS slipping to 29% is still higher than how much debt a household’s income serviced in the 1990s.

Source: Statistics Canada, Canadian Real Estate Association (CREA), Canada Mortgage and Housing Corporation (CMHC). AI-generated 3D bars in infographic showing trendline of household GDS% and 3D bars of price-to-annual-household-income multiple for each year from 1990 to 2026.

The Perfect Storm: Why did house prices explode?

The unnatural spike that hit the market between 2020 and 2025 was the result of a ‘perfect storm’. Overlapping economic and policy events that ignited a buying frenzy.

1. Record low interest rates

During the 2010s and specifically during the 2020 Covid-19 crisis, central banks slashed interest rates to historic, rock-bottom lows. Cheap borrowing fueled a surge in purchasing power, allowing buyers to take on larger mortgages with low monthly carrying costs. This directly drove up asset prices.

2. Covid-19 lockdown effect

COVID-19 lockdown policies restricted international travel and forced Canadians into their homes. With vacations cancelled and as remote work became the norm, discretionary income was redirected into real estate. Available capital triggered a wave of home renovations, up-sizing to larger suburban homes, and a surge in buying cottages or secondary properties.

3. Global capital and foreign investment

Canada’s real estate market became a premier global safe haven for foreign capital. Similar to Australia, New Zealand, and parts of the U.S., significant international wealth—particularly capital flight from China and other nations—flowed directly into Canadian property. For many global investors, buying property wasn't about securing housing; it was about treating Canadian real estate as a politically stable safety deposit box to park their money. As home prices soared, domestic buyers were left at a huge disadvantage.

In June 2022, the federal government passed the Prohibition on the Purchase of Residential Property by Non-Canadians Act that banned foreign investors from buying non-recreational residential property in Canada. The Act came into effect on Jan. 1, 2023 and was extended a year later to Jan. 1, 2027. The move may have been too little too late as house prices have continued to climb higher.

4. Immigration demand shock

In a condensed three-year window, Canada brought in over 3.5 million new residents. While population growth is a standard economic driver, importing millions into a country not building anywhere near enough housing to accommodate them created a demand shock. This misalignment between population influx and housing supply caused an unprecedented buying and renting frenzy.

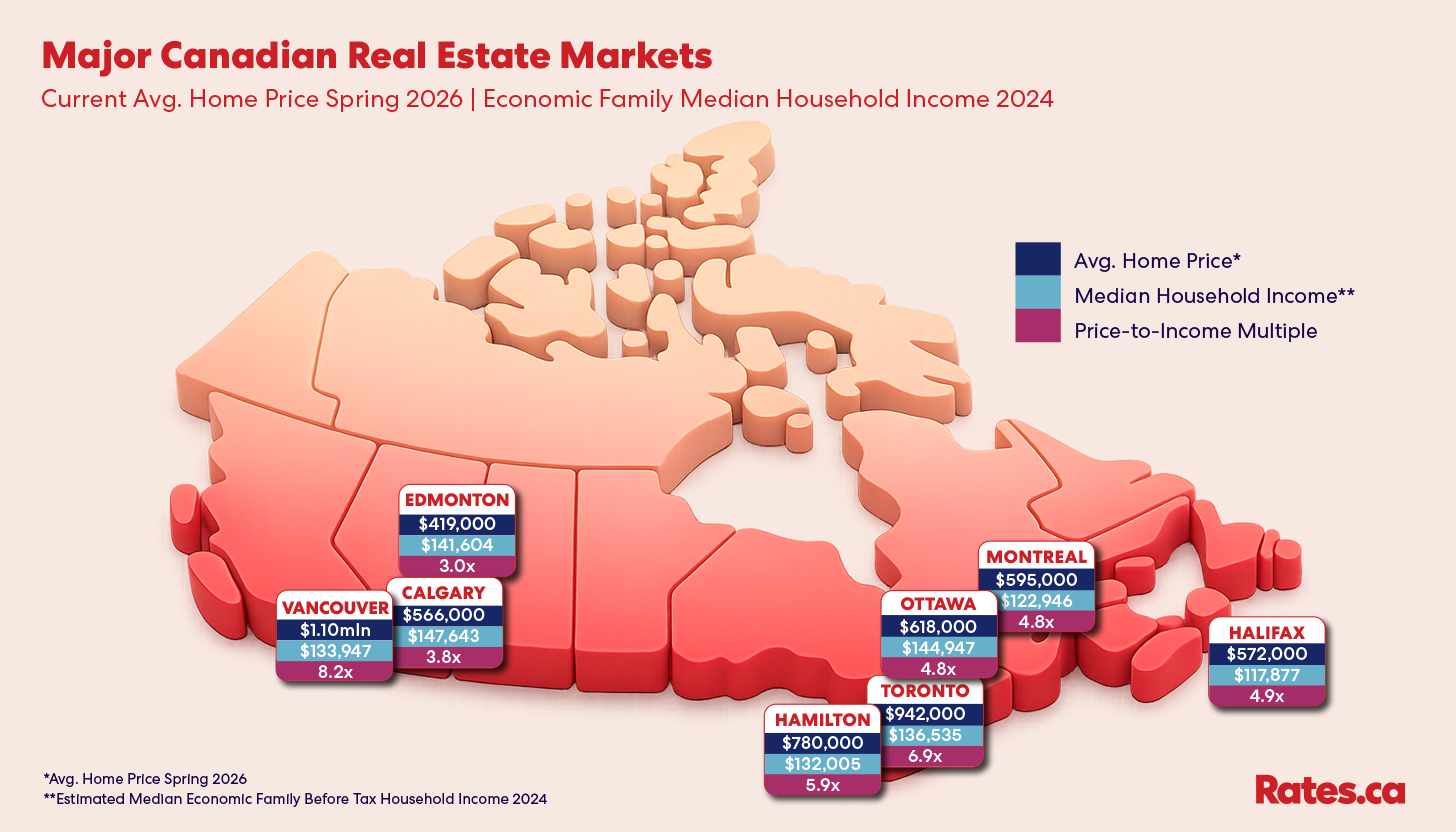

Which Canadian cities are least affordable in 2026?

National averages tend to hide localized pain. The map shows actual, avg. house prices as of Spring 2026 in major metropolitan markets in Canada. Comparative estimates for median economic family before-tax household incomes indicate greater stress on families in Vancouver, Toronto, and Hamilton based on elevated avg. home prices. Even with factoring in a 2.1% year-over-year annual avg. CPI for 2025, and 2.8% YoY inflation in April 2026, median household income increases likely haven't kept pace with real estate price surges.

Source: Statistics Canada, Canadian Real Estate Association (CREA), Canada Mortgage and Housing Corporation (CMHC). AI-generated infographic showing map of Canada and major cities with avg. home price as of Spring 2026, estimated median economic family before tax household income 2024, and price-to-income multiple.

Is Canadian housing more affordable in 2026 than prior years?

Significant debt service costs makes Canadian housing less affordable in 2026 compared to the early 1990s. The fundamental contract of the Canadian middle class used to be: get a good education, find a reliable job, save diligently, and you can own a home in your community. We have transitioned from a real estate market based on what you earn, to a market based on what you (or your parents) already own.

While a 12% borrowing rate in 1990 was painful, principal debt required only $9,300 a year to service. Today, even after a slight market correction, a 4.75% rate on a modern mortgage requires over $32,000 a year to service. You can eventually refinance out of a high interest rate, but you cannot escape a steep purchase price.

Is it better to rent or buy a home in Canada now?

If you can find a way into the real estate market, buying is still better than renting. It is easy to justify $19,200 of annual rent over $32,000 in annual mortgage costs and think, "I'll just rent and invest the difference." But that ignores long-term financial security of homeownership. When you rent, your housing security is entirely at the mercy of a third party. Landlords sell rentals or move family members into properties. Renters can be forced back into the open market, and face inflated rents.

When you buy a home, you are buying a 25-year hedge against inflation. Yes, interest rates fluctuate, but your principal is locked in. Every month, a portion of your payment acts as a forced savings account. In 15 years, while renters are battling ever-increasing market rates, your mortgage payment will likely remain relatively stable, and eventually, you will pay it off.

How Canadians can afford to buy a home in today's market

To fix this crisis of home affordability, we need serious interventions: an increase in housing supply, municipal zoning reform, and economic productivity that drives actual wages up so that our GDS ratios can settle to historic norms.

If you are trying to buy a home today, don’t borrow the absolute maximum that the bank stress-tests you for. Consider duplexes where you can rent out the basement, and protect your cash flow. Above all, don't give up on owning.

Compare Mortgage Rates

Engaging a mortgage broker before renewing can help you make a better decision. Mortgage brokers are an excellent source of information for deals specific to your area, contract terms, and their services require no out-of-pocket fees if you are well qualified.

Here at Rates.ca, we compare rates from the best Canadian mortgage brokers, major banks and dozens of smaller competitors.

Steve Garganis

Steve Garganis, Lead mortgage planner at Mortgage Architects

Steve Garganis is a licensed mortgage broker, leader mortgage planner at Mortgage Architects and founder and editor of CanadaMortgageNews.ca.

In 1992, Steve was one of the first Mobile Mortgage Specialists at TD Bank and has since held senior management positions in two major banks.

In 2004, he decided to focus on his passion for mortgages became a mortgage broker.

In 2009, after noticing a lack of accurate, fact-checked and helpful mortgage content available online at the time, he founded CanadaMortgageNews.ca, where he has written over 600 articles and shares useful facts, opinions and recommendations for the owners, buyers, and sellers.

Featured Topics

Risk tolerance is a lens by which you assess financial trade-off between possible stability with lower returns vs. potential upside involving higher risk.

Buying a home in Canada? Learn the difference between a deposit and down payment, plus minimum payout rules when deal closes.

The Bank of Canada is holding rates for the sixth consecutive time as weak growth and volatile oil prices keep policymakers on the sidelines.

In the summer of 2026, across several regions, Canada's cottage market presents a buying opportunity absent over the last two decades.

Here's a guide to when you might consider using either a mortgage or HELOC, both loans tied to the value of your home.

As the real estate market fluctuates, doing minor, strategic renovations may help improve your home equity and offset falling home values.

From debt ratios to a responsible borrowing history, here are strategies to improve chances of approval of your mortgage application by a Canadian lender.

Bank of Canada holds rates at 2.25% as weak growth clashes with oil-driven inflation. Housing, jobs, and consumer costs show signs of softening.

Learn about pitfalls and benefits of early mortgage renewal, how blended rates work, and why switching lenders could reduce your borrowing costs.