Choose an Insurance Quote

Canadian Mortgage Payments Near Record High: Affordability Under Pressure

If you’re a homebuyer and the explosion in Canadian housing prices has you worried, you’re not alone.

Prices have rallied steeply in recent months, and that’s a problem — for young buyers who need a mortgage, that is.

The combination of record-high home values and a stubborn stress test rate that just won’t fall is hurting housing affordability...a lot. That's despite plunging discounted mortgage rates.

In fact, based on Canada’s minimum stress test rate, the average new buyer's mortgage payment is higher than it’s ever been.

Explainer: The minimum stress test rate is the government-mandated interest rate that lenders make you prove you can afford to get approved for a mortgage.

Fortunately for most people, individual incomes have also risen a bit (based on StatsCan hourly wages). That offsets some of the theoretical payment increase in recent years. That is, for people who still have a job.

That last point can’t be taken for granted, by the way. In its latest Housing Assessment Report, the Canada Mortgage and Housing Corporation (CMHC) noted that disruptions caused by the pandemic have “weakened some of the fundamental determinants [of housing prices],” primarily steep declines in employment and hours worked, which lowered income in most regions. Those lower incomes are dashing the dreams of mortgage approval for hundreds of thousands of Canadians as we speak.

On a share of income basis, the average mortgage payment is still below the last peak in April 2017. So that's a small positive, albeit of little consolation for young homebuyers. (Note: Rates.ca calculates average payments over time based on typical 5-year fixed mortgage rates, CREA’s national average home price and a 20% down payment.)

Compare Mortgage Rates

Engaging a mortgage broker before renewing can help you make a better decision. Mortgage brokers are an excellent source of information for deals specific to your area, contract terms, and their services require no out-of-pocket fees if you are well qualified.

Here at Rates.ca, we compare rates from the best Canadian mortgage brokers, major banks and dozens of smaller competitors.

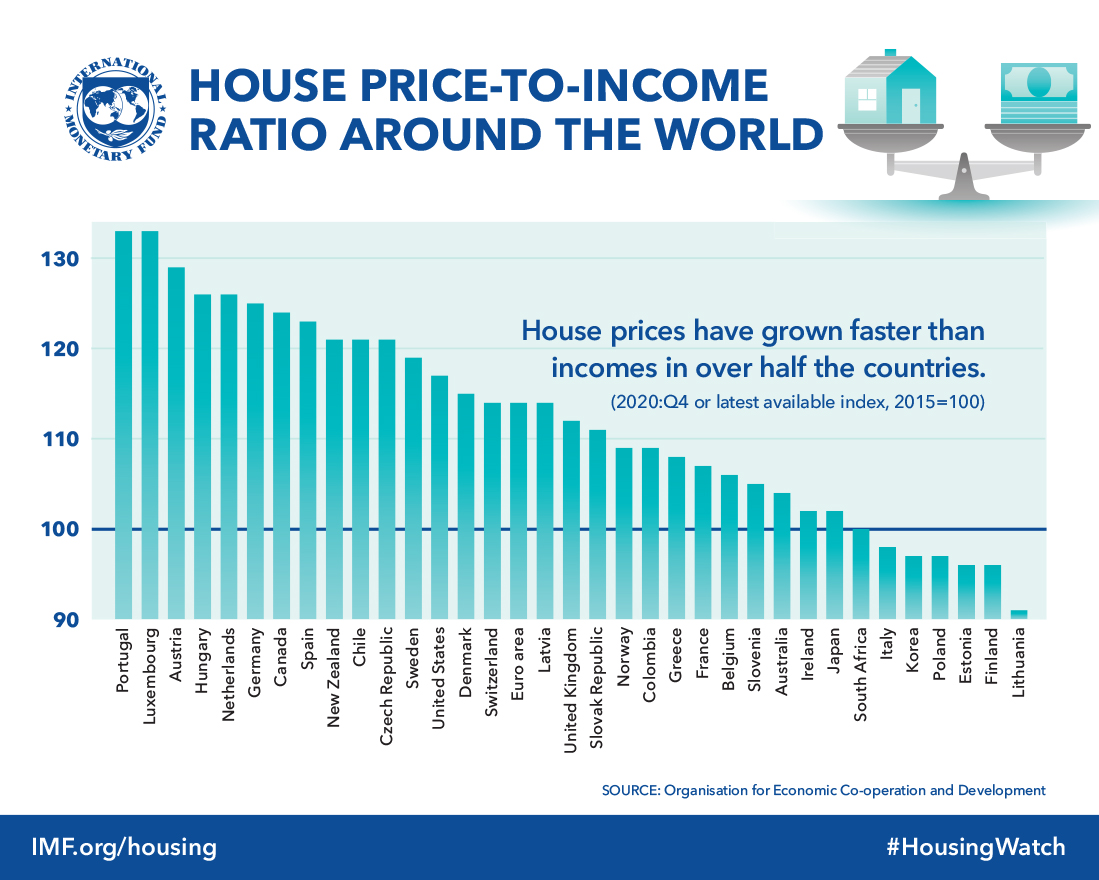

Relative Unaffordability on a Global Scale

Worldwide, Canada ranks towards the upper end of the house-price-to-income measure as reported by the International Monetary Fund. We’re sitting at 111%. Luxembourg is at the high end at 128%, while Italy is near the bottom at 92%. (A villa in Tuscany, anyone?)

{kind=link}

Coincidentally or not, CMHC has sounded alarm bells in its recent affordability assessment. The agency wrote that there’s evidence of “moderate housing vulnerability” at the national level. It said there were signs of overheating in Hamilton, Ottawa, Montreal, Quebec City and Moncton, as of the second quarter of the year. There were also moderate signs of overvaluation in Victoria, Moncton and Halifax. Not only does that have many homebuyers paying extreme prices, but it's increasing their risk at the same time — e.g., if prices correct in 2021 and they lose some/all of their income.

“The evidence of rising imbalances in some local housing markets coupled with the general weakening of housing market fundamentals results in a moderate degree of overall vulnerability being maintained for the Canadian housing market,” the report reads.

On the Plus Side

“In line with action taken by the Bank of Canada in March to support the economy, the nominal 5-year mortgage rate declined” this year, CMHC noted.

Despite an 18.5% explosion in home values year-over-year, that’s kept the typical new homebuyer’s mortgage payment at an estimated $2,471, just below the April 2017 peak of $2,480. Not much of a silver lining but it's something.

Rob McLister

Rob McLister,

Rob McLister has been informing mortgage consumers and professionals since 2007. In that time, he's written more than 2,500 mortgage stories for publications ranging from the Globe and Mail where he presently serves as mortgage columnist to the National Post, Macleans, Canadian Mortgage Trends and RateSpy.com. Regularly quoted throughout the media, Rob is a committed advocate of greater transparency in the mortgage industry. He's also been a vocal consumer advocate for more sensible mortgage regulation. In 2011, he launched two mortgage fintechs: mortgage comparison website RateSpy.com and digital mortgage broker intelliMortgage Inc. The former is the go-to source of Canadian mortgage news and the only site comparing all publicly advertised prime mortgage rates. The latter is Canada's leading online mortgage provider for self-directed borrowers. Both companies were acquired in 2019 by Rates.ca Group Ltd.

Featured Topics

Reverse mortgages can unlock home equity for older Canadians but be aware of risks and high borrowing costs.

Home sellers in Canada must disclose latent defects, hidden property issues, and potential legal risks.

Risk tolerance is a lens by which you assess financial trade-off between possible stability with lower returns vs. potential upside involving higher risk.

Buying a home in Canada? Learn the difference between a deposit and down payment, plus minimum payout rules when deal closes.

The Bank of Canada is holding rates for the sixth consecutive time as weak growth and volatile oil prices keep policymakers on the sidelines.

In the summer of 2026, across several regions, Canada's cottage market presents a buying opportunity absent over the last two decades.

Here's a guide to when you might consider using either a mortgage or HELOC, both loans tied to the value of your home.

As the real estate market fluctuates, doing minor, strategic renovations may help improve your home equity and offset falling home values.

From debt ratios to a responsible borrowing history, here are strategies to improve chances of approval of your mortgage application by a Canadian lender.